Starting October 1, 2025, the National Pension System (NPS) will undergo its most significant reforms yet. Key changes include:

- 100% equity allocation for non-government subscribers.

- Multiple Scheme Framework (MSF) allows more than one scheme under a single PRAN.

- Revised CRA charges for account maintenance.

- Proposed new withdrawal rules: early exit after 15 years, reduced annuity to 20%, higher lump-sum withdrawals, and the introduction of Systematic Unit Redemption (SUR).

These updates make NPS more flexible, liquid, and appealing; however, they also raise important concerns regarding risk, retirement security, and tax efficiency.

Major Changes in NPS (Effective October 2025)

1. 100% Equity Allocation for Non-Government Subscribers

- Before: Equity investment was capped (generally 50–75%).

- After: Non-government subscribers (all citizens, corporates, self-employed) can allocate 100% of their NPS contributions into equity (E asset class).

Why It Matters:

- Young investors can maximize long-term compounding.

- But high equity exposure increases volatility not ideal for those nearing retirement.

2. Multiple Scheme Framework (MSF)

- Before: One scheme per tier under one CRA (Central Recordkeeping Agency).

- After: A single PRAN can now hold multiple schemes across CRAs.

Impact:

- Greater flexibility in diversifying investments.

- Easier switching between CRAs and schemes.

- Encourages competition among fund managers, leading to better performance and service.

3. Revised CRA Charges

- Effective Oct 1, 2025, CRA (account maintenance) fees are being updated for NPS, NPS Vatsalya, UPS, and APY.

- Charges vary by subscriber type (government vs private) and mode (online vs offline).

What You Should Do:

- Track new fee structures to see how they affect your returns.

- Prefer online transactions to minimize costs.

Proposed Exit & Withdrawal Rule Changes (Draft, Awaiting Approval)

These are in the exposure draft stage (final notification pending). If approved, they will revolutionize withdrawal flexibility.

1. Early Exit After 15 Years

- Before: Exit was mostly allowed only at 60 (or retirement).

- Proposed: Subscribers may exit after 15 years (scheme-dependent).

Example: A 35-year-old joining NPS in 2025 could exit by age 50 instead of waiting till 60.

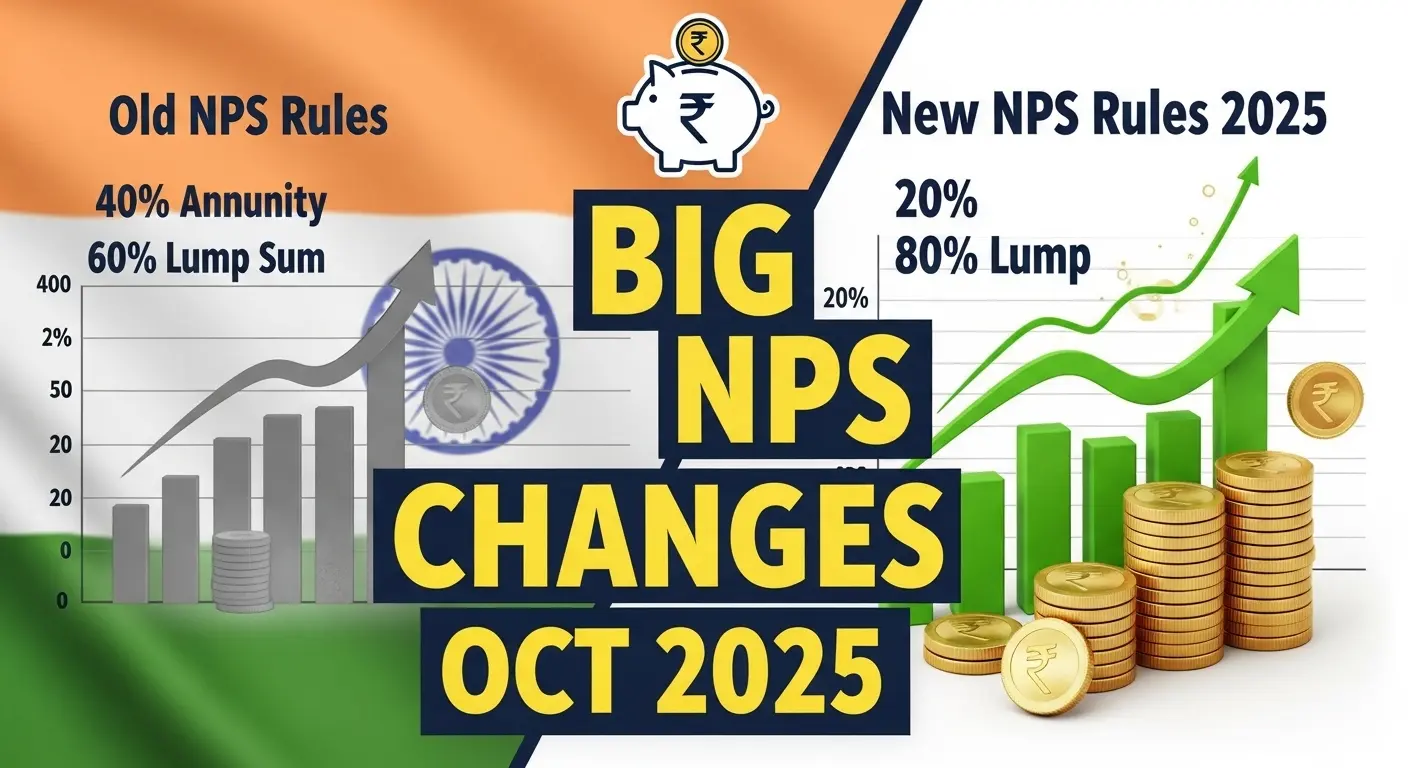

2. Reduced Mandatory Annuity Requirement

- Before: 40% of corpus had to go into annuity.

- Proposed: Only 20% mandatory annuity, rest can be withdrawn.

Impact:

- More cash in hand, less locked into low-return annuities.

- But less guaranteed lifelong income.

3. Higher Lump-Sum Withdrawals

- Before: Lump-sum capped at 60%.

- Proposed: Up to 80% lump-sum allowed in many cases.

- For a smaller corpus (≤ ₹12 lakh): up to 50% lump sum, balance via annuity or SUR.

4. Introduction of Systematic Unit Redemption (SUR)

- Works like a Systematic Withdrawal Plan (SWP) in mutual funds.

- Lets you withdraw periodically while the rest of your corpus stays invested.

Why It’s Useful:

- More flexible than an annuity.

- You stay invested for growth while drawing income.

5. Extended Deferment Till Age 85

- Subscribers can delay exit/withdrawals up to age 85.

- Useful for those who want to remain invested longer or delay pension start.

6. Loan / Lien Facility

- Subscribers can pledge their NPS corpus for loans from regulated institutions.

- Adds a safety net for emergencies.

7. UPS to NPS Switch (Government Employees)

- Central government employees under the Unified Pension Scheme (UPS) may get a one-time, one-way switch to NPS (with conditions).

NPS Before vs After (Comparison Table)

| Feature | Before | After (Oct 2025 / Proposed) |

|---|---|---|

| Equity Allocation | Max 50–75% | Up to 100% |

| Scheme Choice | 1 scheme per CRA | Multiple schemes under MSF |

| Exit Age | Typically 60+ | 15 years investment (if scheme allows) |

| Mandatory Annuity | 40% | 20% (proposed) |

| Lump-Sum Withdrawal | 60% | Up to 80% |

| Withdrawal Modes | Lump sum + annuity | SUR + annuity mix |

| Maximum Deferment | Till ~70 | Till 85 |

| Loan Against NPS | Not allowed | Allowed |

| CRA Charges | Existing rates | 15-year investment (if scheme allows) |

NPS Before vs After Calculator — Oct 2025 Rules

Compare old vs new NPS rules (Oct 1, 2025): lump-sum, annuity corpus, estimated pension and SUR income. Change inputs to see instant numeric & visual comparisons.

Results — Instant Comparison

Old Lump Sum

Old Annuity Corpus

Estimated Old Annual Pension

New Lump Sum

New Annuity Corpus

Estimated New Annual Pension

Difference — Immediate Cash

Difference — Annual Pension

SUR Monthly Estimate

Notes

Practical Example: Before vs After

Case: Ravi, 35 years old, invests ₹12,000/month. After 15 years, corpus = ₹30 lakh.

- Before:

- No exit until age 60.

- At 60, max 60% (₹18 lakh) lump sum, 40% (₹12 lakh) annuity.

- Limited flexibility.

- After (Proposed Rules):

- Could exit at 50 (after 15 years).

- Withdraw up to 80% (₹24 lakh) lump sum.

- Only 20% (₹6 lakh) annuity.

- Or opt for SUR: monthly withdrawals while keeping the corpus invested.

Ravi gains liquidity and control but loses the safety of a bigger lifelong pension.

Benefits of the 2025 Reforms

- Greater investment choice (100% equity).

- Early access to funds after 15 years.

- Higher lump-sum withdrawals.

- Flexible income through SUR.

- The loan option adds emergency support.

- More competitive fund management via MSF.

Risks & Caveats

- Market Risk: 100% equity = higher volatility.

- Longevity Risk: With a lower annuity, the risk of outliving savings rises.

- Behavioral Risk: Easy withdrawals may tempt premature spending.

- Regulatory Risk: Draft rules may still change.

- Fee Impact: Higher CRA charges could dent net returns.

FAQs on NPS Changes October 2025

Equity, MSF, CRA charges = final (from Oct 1, 2025).

Exit/withdrawal rules = draft, pending approval.

Only if your scheme adopts this provision.

Systematic Unit Redemption – like a mutual fund SWP, periodic withdrawals while staying invested.

No major tax changes announced yet. The current EET (Exempt-Exempt-Tax) framework continues.

Only if young, risk-tolerant, and long-term oriented. Near-retirement investors should balance with safer assets.

Final Thoughts

The October 2025 NPS reforms mark a turning point in India’s retirement planning landscape. With full equity access, early exits, reduced annuity, SUR withdrawals, and more flexibility, NPS is evolving from a rigid pension product to a more modern investment tool.

But greater freedom also brings greater responsibility. To make the most of these reforms:

- Young investors should balance growth (equity) with safety (debt).

- Mid-career subscribers should avoid premature exits that could harm retirement security.

- Retirees should explore SUR carefully for income flexibility.

In short, NPS is becoming more powerful, but you must use it wisely.