A complete comparison of SIP mutual fund investing and ULIP for 2026. Covers charges, lock-in, liquidity, insurance cover, fund switching, and taxation, so you can decide which one actually fits your goal: pure wealth creation or a combined insurance-investment product.

SIP and ULIP both let you invest in the market in small, regular instalments, but they are built for different purposes. A SIP is a way of investing in a mutual fund; a ULIP is an insurance policy with a market-linked investment component attached. Comparing them directly only makes sense once you separate what each product is actually solving for.

This guide compares both on cost, flexibility, insurance, taxation, and returns, and gives you a practical way to decide which one, or which combination, fits your situation in 2026.

Quick Answer: If your goal is pure wealth creation, a SIP in a mutual fund is usually more efficient due to lower charges and full liquidity. If you specifically want life cover bundled with market-linked investing in a single product, and you can commit to the five-year lock-in, a ULIP can work, though buying term insurance separately and investing the difference through SIP is typically cheaper for the same protection.

What Is a SIP

A Systematic Investment Plan is simply a method of investing a fixed amount into a mutual fund at regular intervals, usually monthly. It is not a separate product; it is how you invest in the mutual fund scheme you choose, whether equity, debt, or hybrid. Returns depend entirely on the fund’s performance minus its expense ratio.

What Is a ULIP

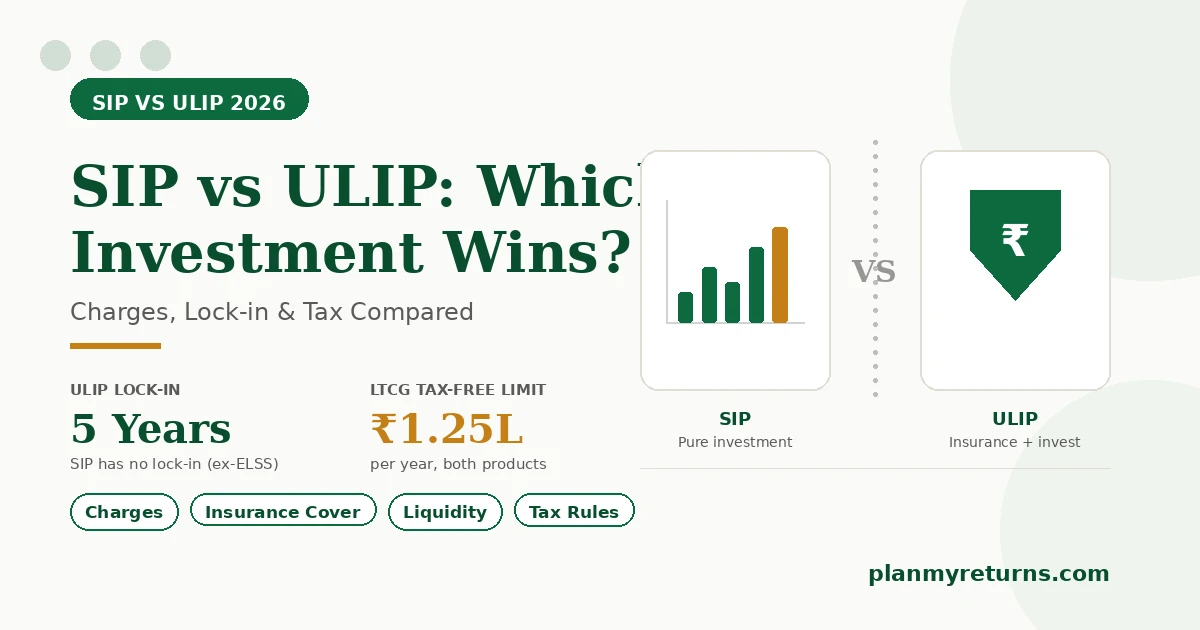

A Unit Linked Insurance Plan is a life insurance policy where part of your premium buys life cover and the rest is invested in market-linked funds you select, similar to mutual fund options. ULIPs carry a mandatory five-year lock-in and typically involve several layers of charges not present in a mutual fund: premium allocation charges, policy administration charges, fund management charges, and mortality charges for the life cover.

SIP vs ULIP: Side-by-Side Comparison

| Factor | SIP (Mutual Fund) | ULIP |

|---|---|---|

| Primary purpose | Wealth creation only | Insurance plus investment |

| Lock-in period | None for open-ended funds (ELSS: 3 years) | 5 years mandatory |

| Life insurance cover | Not included | Included, chosen at purchase |

| Typical charges | Expense ratio only, roughly 0.5-1% for direct plans | Premium allocation, admin, mortality, and fund management charges, often 1.5-3%+ in early years |

| Fund switching | Treated as redemption plus new purchase, capital gains tax applies | Free switches within the policy, no capital gains tax on switching |

| Liquidity | High, redeem anytime (exit load may apply short-term) | Low, locked for 5 years, partial withdrawal allowed after that within limits |

| Transparency of charges | High, expense ratio disclosed daily | Moderate, multiple charge heads spread across the policy term |

| Tax deduction on contribution | Only ELSS qualifies under Section 80C | Premium qualifies under Section 80C, subject to the 10% of sum assured condition |

| Maturity taxation | LTCG above ₹1.25 lakh taxed at 12.5%; STCG at 20% | Tax-free under Section 10(10D) if annual premium ≤ ₹2.5 lakh; otherwise taxed like an equity fund |

Charges: Where ULIP Loses Ground Early On

Mutual fund SIPs charge a single, disclosed expense ratio deducted from the fund’s NAV daily. ULIPs layer several charges on top of each other, especially in the first few years: a premium allocation charge that can eat a meaningful chunk of early premiums, a policy administration charge, a fund management charge similar to an expense ratio, and a mortality charge for the insurance component that rises with age.

Why this matters: Because several ULIP charges are front-loaded, the effective cost in the first two to three years is meaningfully higher than a comparable mutual fund SIP, even though newer ULIPs have reduced these charges compared to older-generation policies. Over a long enough horizon, lower ongoing charges compound in your favour, which usually favours a plain SIP for pure wealth creation.

Lock-in and Liquidity

An open-ended mutual fund SIP has no lock-in beyond ELSS, which locks each instalment for three years. You can pause, stop, increase, or redeem a SIP at any time, subject only to a short-term exit load on some schemes.

A ULIP locks you in for five years by regulation. Stopping premiums within this period moves the policy into a discontinuance fund, insurance cover typically lapses, and you only receive the discontinuance value after the lock-in ends, reduced by a discontinuance charge. This makes a ULIP a poor fit if you are not confident you can sustain premiums for the full term.

Insurance Cover: The One Thing ULIP Offers That SIP Doesn’t

A SIP provides zero life cover. If the investor passes away, the fund units simply pass to the nominee at current value, with no additional payout. A ULIP includes a sum assured, so the nominee typically receives the higher of the fund value or the sum assured, or in some structures, the fund value plus the sum assured, depending on the policy design.

For most people, buying a separate term insurance policy for protection and investing the rest through SIP works out cheaper than a ULIP offering similar cover, because term insurance is priced purely for mortality risk without an investment layer attached.

Taxation: SIP vs ULIP in 2026

Equity mutual fund SIP gains are taxed as capital gains. Units held over 12 months qualify for long-term capital gains treatment, with the first Rs 1.25 lakh of gains in a financial year exempt and anything above taxed at 12.5%. Units held 12 months or less are taxed as short-term capital gains at 20%. Each SIP instalment has its own purchase date, so a single redemption can include both short-term and long-term units.

ULIP maturity proceeds remain fully tax-exempt under Section 10(10D) only if your total annual premium across all ULIPs stays within Rs 2.5 lakh and the premium does not exceed 10% of the sum assured. If you cross that threshold, the policy loses its exempt status and maturity gains are taxed the same way as an equity mutual fund. Death benefit payouts remain tax-free regardless of premium size.

Advantage ULIP: Switching between equity and debt funds inside a ULIP triggers no capital gains tax, since the switch happens within the insurance wrapper. Doing the same in mutual funds means redeeming one scheme and buying another, which is a taxable event on any gains from the redeemed units.

Want to see how SIP returns actually add up over time? Project your investment growth with your own numbers.

Try the SIP CalculatorHow to Decide: A Practical Approach

Separate Insurance From Investment First

Decide your life insurance need independently of your investment plan. If you have dependents, buy adequate term insurance regardless of which investment product you eventually choose.

Check Your Ability to Commit for 5+ Years

Only consider a ULIP if you are confident you can sustain premiums through the five-year lock-in without needing that money for an emergency. If your income or cash flow is uncertain, a SIP’s flexibility matters more.

Compare Effective Cost, Not Just the Headline Return

Ask for the ULIP’s charge structure in writing, including premium allocation, fund management, and mortality charges, and compare the effective annual cost against a mutual fund’s expense ratio over your intended holding period.

Decide Based on Goal, Not Tax Deduction Alone

Both ULIP premiums and ELSS mutual fund investments qualify for Section 80C. Since ELSS has a shorter three-year lock-in and typically lower charges, do not choose a ULIP purely to claim the deduction; choose it only if you genuinely want the bundled insurance-investment structure.

Decision Checklist Before You Choose

- Confirm you already have, or will separately buy, adequate term life insurance regardless of which product you pick

- Confirm you can sustain ULIP premiums for the full 5-year lock-in without needing the funds earlier

- Confirm the ULIP’s total charge structure, not just the headline fund performance, before committing

- Confirm whether frequent fund switching matters to you, since ULIP offers this tax-free and mutual funds do not

- Confirm your total annual ULIP premium, if you choose one, stays within Rs 2.5 lakh to preserve the tax-free maturity benefit

- Run both options through a calculator using your actual numbers rather than comparing on reputation or an agent’s pitch alone

Frequently Asked Questions

Conclusion

SIP and ULIP are not really competing for the same job. A SIP is the more efficient tool for pure wealth creation, thanks to lower charges, full liquidity, and daily transparency. A ULIP earns its place only when you specifically want insurance and investment bundled together and can commit to the five-year lock-in. For most people, buying term insurance separately and running a disciplined SIP alongside it delivers both better protection and better returns than a single ULIP.

Project your potential SIP growth with the SIP Calculator, compare a one-time investment using the Lumpsum Calculator, and check your capital gains tax liability on redemption with the Capital Gains Calculator before you decide.