For years, Indian parents and planners have poured money into mutual funds with comforting names like “Children’s Gift Fund” or “Retirement Savings Fund”. They felt safe. They felt purposeful. But under the hood, many of these funds were just standard equity or hybrid funds wrapped in emotional marketing.

To clean up the industry, reduce portfolio overlap, and make investing truly “true to label”, SEBI stepped in. As of February 26, 2026, the old way of goal based mutual fund investing is officially over. Here is everything you need to know about the transition and how to handle your money moving forward.

The Big News: What Exactly Did SEBI Change?

SEBI has officially scrapped the “Solution Oriented Schemes” category. This means fund houses can no longer accept fresh money into their existing retirement and children’s mutual funds.

Why did they do this? In the past, you might have invested in a Children’s Fund and a regular Flexi Cap fund, not realizing that both funds were buying the exact same stocks. You thought you were diversifying, but you were just duplicating your risk. SEBI wants to stop this confusion. They want you to know exactly what you are buying.

Is My Money Safe? What Happens to My Existing SIPs?

This is the most common question investors are asking right now. Yes, your money is 100 percent safe.

Here is exactly what happens next:

- Immediate Stop on New Money: If you have an active Systematic Investment Plan (SIP) in one of these discontinued funds, fresh subscriptions are halted immediately.

- The Grand Merger: Fund houses cannot just keep your old fund running in isolation. They are required to merge these discontinued schemes with another existing fund that has a similar risk profile and asset allocation.

- Regulatory Approval: Your mutual fund company cannot do this randomly. They must get prior approval from SEBI before moving your money.

If you were relying on a specific fund to estimate your child’s future education costs, you might want to recalculate your targets using a reliable SBI children’s fund calculator or a similar tool to see where your current accumulated corpus stands.

The Game Changer: Say Hello to Life Cycle Funds

SEBI did not just take away your old options; they replaced them with something much better. Welcome to the era of “Life Cycle Funds.”

If you are familiar with the National Pension System, you might already know how this works. (If you are curious about how NPS compares, you can always run your numbers through an NPS calculator).

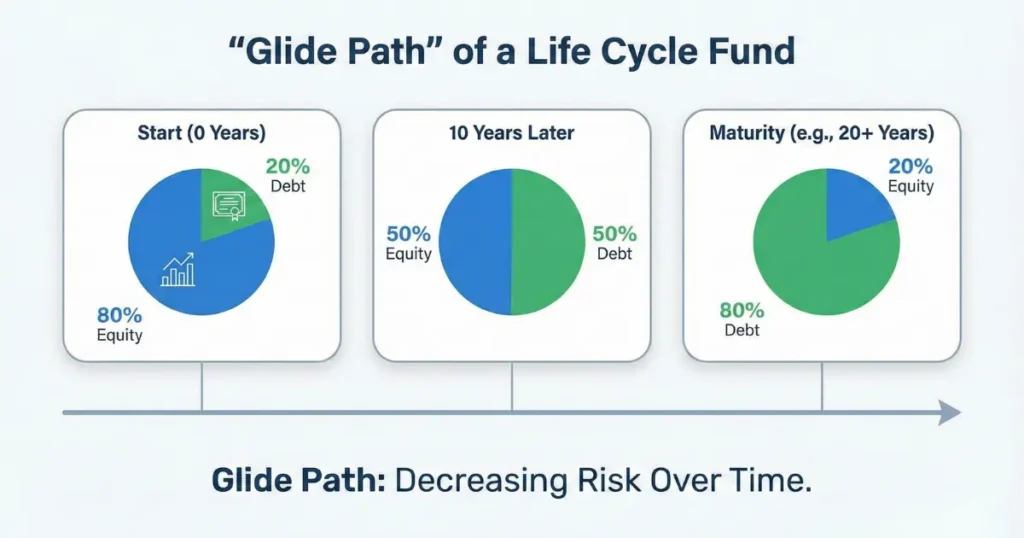

A Life Cycle Fund is an open ended mutual fund with a specific maturity year attached to its name, such as “Life Cycle Fund 2045”. These funds use a strategy called a “glide path.”

Think of a glide path like driving a car on a highway.

- The Early Years (High Speed): When your goal is 15 or 20 years away, the fund invests heavily in equity (stocks) to give you maximum growth.

- The Middle Years (Cruising): As you get closer to your target year, the fund manager automatically starts moving your profits from risky equities into safer debt instruments.

- The Final Years (Slowing Down): By the time your goal arrives, your money is mostly parked in highly secure, low volatility assets.

This is brilliant because it removes human emotion. You do not have to guess when to sell your stocks to protect your profits before your child goes to college or before you retire. The fund does it for you automatically.

Important Rules for Life Cycle Funds

- Maturity Options: You can pick funds with target maturities ranging from 5 years up to 30 years (in multiples of 5).

- Strict Exit Loads: To keep you disciplined, SEBI has enforced strict exit penalties. If you withdraw your money in the first year, you pay a 3 percent exit load. It drops to 2 percent in the second year, and 1 percent in the third year. This ensures these funds are used for actual long term planning, not quick trading.

Value vs. Contra Funds: More Choices, Less Clutter

Aside from goal based investing, SEBI also cleaned up standard equity funds. Previously, a mutual fund house could only offer either a Value Fund or a Contra Fund. Now, they can offer both.

However, there is a catch. SEBI mandated that the portfolio overlap between the two funds cannot exceed 50 percent.

What does this mean in plain English? A Value Fund looks for good companies whose stock prices are temporarily cheap. A Contra Fund bets against the current market trends, buying sectors that everyone else is ignoring. SEBI is simply ensuring that if a fund house offers both, they are genuinely using two different strategies, rather than selling you the same stocks under two different names.

What Should You Do Next?

If you are holding a discontinued Retirement or Children’s fund:

- Wait for Communication: Your mutual fund company will send you an email detailing which scheme your money is being merged into.

- Review the New Scheme: Check if the new merged fund aligns with your original risk appetite.

- Plan Your Next Move: If you do not like the new merged fund, you can withdraw your money and reinvest it into a brand new Life Cycle Fund that perfectly matches your target year. If you are planning for retirement, use a dedicated retirement calculator to figure out exactly which target year fund (like 2040 or 2050) you need to buy.

Frequently Asked Questions

No, Life Cycle Funds are taxed based on their asset allocation at the time of withdrawal. If the fund is heavily invested in equity (over 65 percent), it will be taxed like an equity fund. As the fund shifts towards debt closer to maturity, the taxation rules may align more with debt fund taxation. Always consult your CA for precise calculations upon maturity.

Yes, you can stop your SIP payments at any time without any penalty. However, if you withdraw the accumulated money within the first three years, you will face the strict exit loads mentioned earlier (up to 3 percent).

No, you will not lose the value of your investments. Your existing units will be converted into units of the new merged scheme at the prevailing Net Asset Value (NAV). The total monetary value of your investment remains exactly the same on the day of the merger.

To prevent clutter, SEBI has capped it. A single mutual fund house can only have a maximum of 6 active Life Cycle Funds available for subscription at any given time.