If you have ₹10 lakh sitting in your bank, this guide compares Fixed Deposit vs Mutual Fund for Indian investors in 2026 — with real post-tax returns, risk levels, liquidity, and a clear winner for every investor profile.

Should you put your ₹10 lakh in a Fixed Deposit or a Mutual Fund? This is one of the most common money questions Indians ask in 2026. The simple answer: it depends on your time horizon, risk tolerance, and goal. The detailed answer involves understanding post-tax returns, real inflation-adjusted growth, and how much volatility you can stomach.

FDs feel safe. You see your money grow predictably every quarter. But that comfort comes at a cost. Mutual funds feel risky. They go up and down with the market. But over 10 years, they have historically delivered 2x to 3x more wealth than FDs, even after accounting for tax and risk.

In this guide, we run real numbers on both options for FY 2026-27, show you exactly what ₹10 lakh becomes after 10 years in each, and tell you which option suits which investor profile.

Quick rule of thumb: Need the money in 3 years or less? Choose FD. Have a 5+ year horizon and can handle short-term ups and downs? Choose mutual funds. We explain why below.

The ₹10 Lakh Showdown: Side-by-Side Comparison

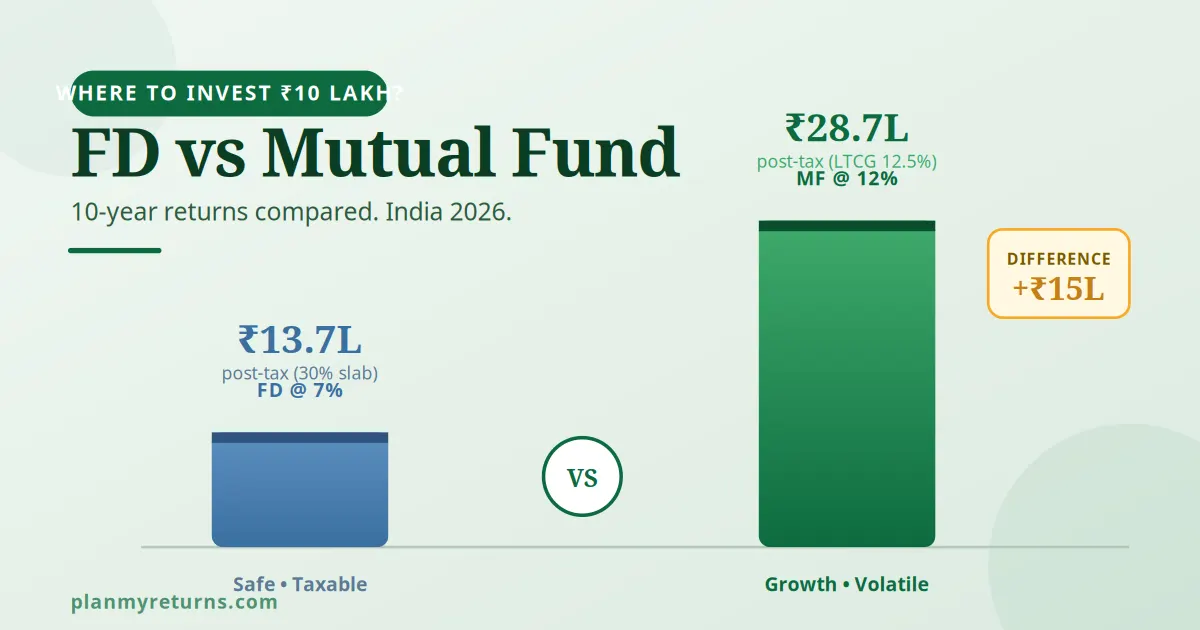

Here is what ₹10 lakh becomes in each option after 10 years, including tax impact:

After 10 years, ₹10 lakh becomes ₹16.77 lakh in FD but ₹28.58 lakh in mutual funds. That is a difference of nearly ₹12 lakh in extra wealth, post-tax.

And that is just for one period. Over 20 years, this gap explodes to over ₹50 lakh.

Calculate your own FD vs MF returns.

Run the exact numbers for your investment amount and tenure.

FD vs Mutual Fund: 8 Key Parameters Compared

Returns are just one piece of the puzzle. Here is how FD and Mutual Fund compare across every parameter that matters for Indian investors:

The Hidden Cost of FDs: Inflation

Here is what most Indians miss when they choose FD. The 7% interest looks great. But after tax (30% slab) and inflation (6%), your real return is barely 1%.

This means your ₹10 lakh in FD loses purchasing power every year. The number on your bank statement grows. But what you can actually buy with that money shrinks. A ₹50 lakh house today will cost ₹89 lakh in 10 years at 6% inflation. Your FD growth cannot keep up.

Equity mutual funds, despite short-term volatility, have consistently delivered 6 to 8% real returns (after inflation and tax) over 10+ year periods in India. Calculate your real returns using the Inflation Calculator.

Real Return Reality Check: ₹10 lakh in FD at 7% becomes ₹19.67 lakh in 10 years. But adjusting for 6% inflation, your purchasing power is only ₹10.98 lakh. You essentially preserved capital, not grew it.

When FD is the Right Choice

Scenario 1: Short-Term Goals (1 to 3 Years)

Need money for a wedding next year? Buying a car in 2 years? Down payment for a house in 18 months?

Choose FD. Equity mutual funds can be down 20% in any year. You cannot risk a short-term goal.

Pick: Fixed DepositScenario 2: Emergency Fund

Your emergency fund (6 months of expenses) needs to be safe and accessible. This is not the place for market risk.

Choose FD or Liquid Fund. A short-tenure FD or liquid mutual fund (debt category) keeps the money safe and accessible. Calculate how much you need with the Emergency Fund Calculator.

Pick: Fixed Deposit / Liquid FundScenario 3: Senior Citizens with No Other Income

If you are retired and depend on this corpus for monthly expenses, capital safety is paramount.

Choose FD or SCSS. Senior citizens get 0.25 to 0.50% extra on bank FDs. SCSS (Senior Citizen Savings Scheme) gives 8.2%. Both are far safer than mutual funds for income generation.

Pick: FD or SCSSScenario 4: You Cannot Sleep at Night

If watching your portfolio drop 15% in a month would make you panic-sell at the bottom, mutual funds are not for you. Investor behavior matters more than returns.

Choose FD. A guaranteed 7% you stay invested in beats a theoretical 12% you panic-exit at 8%.

Pick: Fixed DepositWhen Mutual Fund is the Right Choice

Scenario 1: Long-Term Wealth Creation (5+ Years)

Building corpus for retirement (20-30 years away)? Saving for child’s higher education (15+ years)? Want to become a crorepati?

Choose Equity Mutual Fund (SIP or Lumpsum). Over 10+ years, equity has rarely lost money in India and has dramatically outperformed FD post-tax. Calculate your wealth potential with the SIP Calculator or Lumpsum Calculator.

Pick: Equity Mutual FundScenario 2: Tax Saving Under 80C

Want to save ₹46,800 in tax under Section 80C while building wealth?

Choose ELSS Mutual Fund. ELSS gives the same tax benefit as FD but with potential for 12-15% returns and only 3-year lock-in (vs 5 years for tax saver FD). Use the ELSS Calculator.

Pick: ELSS Mutual FundScenario 3: Regular Income Post-Retirement (with Stable Pension)

Retired but already have pension covering basic expenses? Have a 15+ year horizon?

Choose Hybrid Funds + SWP. Set up SWP (Systematic Withdrawal Plan) for monthly income. Far more tax-efficient than FD interest. Use the SWP Calculator.

Pick: Hybrid MF with SWPScenario 4: Goal-Based Investing

Saving for child’s college (10-15 years), home down payment (7+ years), retirement (20+ years)?

Choose Mutual Fund SIP matched to goal. Use diversified equity funds for long-term goals. Plan with the Education Planning Calculator or Retirement Calculator.

Pick: Equity Mutual Fund SIPThe Smart Strategy: Don’t Choose. Combine Both.

The smartest investors don’t pick FD or mutual fund. They use both, for different purposes. Here is a model split for ₹10 lakh:

The asset allocation rule: Equity allocation = (100 – your age)%. So a 30-year-old should have 70% in equity and 30% in debt/FD. A 60-year-old should flip it: 40% equity, 60% safe instruments. Use the Asset Allocation Calculator to plan yours.

Real Example: Two Friends, Same Salary, Different Choices

Rahul and Amit, both 30, earn ₹15 lakh/year. Both invest ₹10,000/month for 25 years.

Rahul plays it safe. He puts everything in 5-year FDs and rolls them over. Average return: 7%. After 25 years and tax, his corpus: ₹62 lakh.

Amit takes calculated risk. He invests in a diversified equity mutual fund SIP. Average return: 12%. After 25 years and LTCG tax, his corpus: ₹1.71 crore.

The difference: ₹1.09 crore. Same income. Same monthly investment. Same time. Just different vehicles. That is the cost of being too safe with long-term money. Calculate your own scenarios using the SIP Calculator.

Find out what your investment can grow to.

Compare FD, SIP, and Lumpsum returns side by side.

5 Common Mistakes Indians Make

Mistake 1: Putting all retirement money in FD. If you are 30+ years from retirement, FD is the worst option. You are guaranteed to lose to inflation over decades.

Mistake 2: Putting next year’s wedding money in mutual funds. Equity can drop 20% next month. Short-term goals need FD or liquid funds, not mutual funds.

Mistake 3: Ignoring tax on FD interest. A 7% FD in 30% tax slab gives you only 4.9% post-tax. Plan based on post-tax returns, not headline rates.

Mistake 4: Comparing FD with monthly NAV of mutual funds. Mutual funds will go down some months. That is normal. Judge them on 5-7 year periods, not monthly statements.

Mistake 5: Choosing FD because “stocks are gambling.” Diversified mutual funds are not stocks. They invest in 50-100 companies across sectors. Diversification kills the gambling argument.

Plan Your Financial Journey

Whether you choose FD, Mutual Fund, or a smart mix, the key is having a plan. Use these calculators on PlanMyReturns to make informed decisions.

Compare your FD returns with the FD Calculator and RD Calculator. Project mutual fund growth using the SIP Calculator or Lumpsum Calculator. Plan your retirement corpus with the Retirement Calculator. Calculate the impact of inflation on your savings using the Inflation Calculator. Determine your ideal asset mix with the Asset Allocation Calculator.

Explore all free financial calculators at PlanMyReturns Calculators. Every calculation follows transparent methodology and assumptions.

Frequently Asked Questions: FD vs Mutual Fund