The “HR Email” is Here. Don’t Ignore It.

It’s the first Monday of the year. If you are a salaried employee, you likely just received an email from your Finance/HR team with the subject line: “Urgent: Submit Investment Proofs & Tax Regime Selection for FY 2025-26.”

Most people blindly click “Same as Last Year.” In 2026, that is a costly mistake.

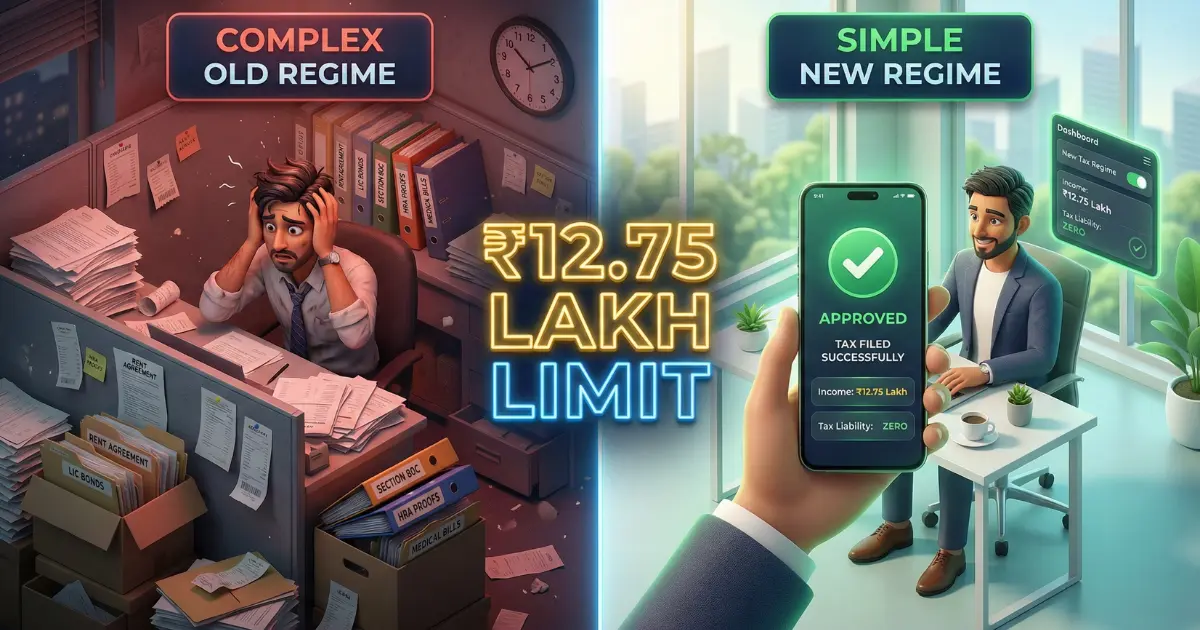

With the New Income Tax Act 2025 now fully operational and the standard deduction hiked to ₹75,000, the math has fundamentally shifted. For 90% of professionals, the “Old Regime” (with its 80C and HRA hassles) is officially dead

Here is the no-nonsense guide to declaring your taxes this week so you don’t see a massive TDS cut in your January 31st paycheck.

The New “Magic Number”: ₹12.75 Lakh

Let’s cut to the chase. The biggest change for the Assessment Year 2026-27 is the effective tax-free threshold.

Under the updated New Tax Regime, if your annual gross salary is ₹12,75,000 or less, your tax liability is ZERO.

The Math:

- Gross Salary: ₹12,75,000

- Less Standard Deduction: ₹75,000

- Net Taxable Income: ₹12,00,000

- Tax Payable: Covered entirely by the enhanced Rebate u/s 87A.

- Final Tax: ₹0

The Implication:

If you earn ₹12.5 Lakh, and you are still struggling to buy LIC policies or lock money in PPF just to save tax under the Old Regime, stop immediately. You are locking up liquidity for no reason. Switch to the New Regime, pay zero tax, and invest that money where it actually grows (like Nifty 50 Index Funds or the 8.05% RBI Bonds).

Old vs. New: The 2026 Break-Even Analysis

“But I have a Home Loan and HRA!”

This is the only valid counter-argument. However, the “Break-Even Point” (the amount of deductions you need for the Old Regime to beat the New Regime) has moved dangerously high.

To make the Old Regime profitable in 2026, you need total deductions exceeding ₹4.25 Lakhs.

Check your own payslip against this list:

- Section 80C: ₹1.5 Lakh (Maxed out)

- Section 80D: ₹25,000 (Medical Insurance)

- Standard Deduction: ₹50,000 (Lower in Old Regime)

- HRA / Home Loan Interest: Do you have ₹2 Lakh+ here?

The Verdict:

Unless you are claiming a massive HRA (paying rent > ₹25k/month) AND paying huge Home Loan interest, the New Regime wins.

| Feature | New Tax Regime (2026) | Old Tax Regime |

| Tax-Free Income | Up to ₹12.75 Lakh | Up to ₹5.5 Lakh |

| Standard Deduction | ₹75,000 | ₹50,000 |

| 80C/80D Benefit | Not Available | Available |

| HRA Exemption | Not Available | Available |

| Documentation | Zero Paperwork | High (Rent receipts, Bills) |

The “Jan-Feb-March” Trap: Why Declaration Matters Now

Why is your HR asking for this today?

Because if you haven’t paid enough tax in the first 9 months of the financial year (April–Dec 2025), your employer is legally required to deduct all pending tax from your remaining 3 paychecks (Jan, Feb, March).

Scenario:

You planned to switch to the New Regime but haven’t told your HR yet. Your HR system is still calculating tax based on the Old Regime (assuming you will submit rent receipts).

- Jan 15th: You fail to upload rent receipts.

- Jan 25th: The payroll software assumes you have NO HRA exemption.

- Jan 31st: It calculates a massive tax liability and deducts 30% of your January salary.

Solution:

Log in to your payroll portal today. If you are switching to the New Regime (which you likely should), select “New Regime” explicitly. This tells the software: “Stop waiting for rent receipts. Just calculate tax on the lower slab rates.”

What to Do This Week (A 3-Step Action Plan)

- Check Your Total Income: Is it under ₹12.75 Lakh?

- Yes? Select “New Regime.” Submit no proofs. Enjoy your full salary.

- No? Go to Step 2.

- Calculate Your “Deduction Efficiency”:

- Add up your actual 80C + 80D + HRA.

- Is the total > ₹4.25 Lakh?

- If Yes -> Stick to Old Regime. Upload your proofs (LIC premium, Rent receipts, School fees) immediately.

- If No -> Switch to New Regime.

- Audit Your Liquidity:

- If you switch to the New Regime, you no longer need to put ₹1.5 Lakh into PPF/ELSS.

- Don’t spend this money. Redirect this “freed-up” cash into a High-Liquidity Asset (like the RBI Floating Rate Bond or a simple Nifty ETF) that isn’t locked for 15 years.

The government wants you to move to the New Regime. The 2026 slabs are designed to make the Old Regime unattractive for everyone except those with very specific, high-deduction heavy financial structures.

Don’t let nostalgia for “Section 80C” cost you money. Do the math, update your HR portal, and save your January paycheck.