An emergency fund is one of the most important parts of personal finance, yet it’s often ignored until a crisis hits. Many people invest regularly, but struggle the moment an unexpected expense appears.

This guide explains what an emergency fund is, how much you really need, how to calculate it correctly, where to keep it, and why it protects your long-term wealth more than any investment return ever could.

If you want to skip straight to numbers, you can use the Emergency Fund Calculator on PlanMyReturns to instantly calculate how much emergency money you should keep based on your monthly expenses and income stability.

What Is an Emergency Fund?

An emergency fund is money set aside specifically to handle unexpected financial situations without disturbing your regular life or long-term investments.

Common emergencies include:

- Job loss or delayed salary

- Medical expenses not fully covered by insurance

- Urgent home or vehicle repairs

- Family emergencies or sudden travel

- Temporary income disruption

This fund is not meant for planned expenses, shopping, vacations, or investments. Its only role is financial protection.

Why an Emergency Fund Is More Important Than Investing

A common mistake is prioritizing investments while ignoring basic financial safety.

Here’s why an emergency fund should come first:

- It prevents forced withdrawals from SIPs, mutual funds, or ULIPs during bad markets

- It avoids high-interest debt like credit cards and personal loans

- It gives you breathing room to make calm decisions under stress

- It protects your credit score and repayment history

Without an emergency fund, even a small setback can undo years of disciplined investing.

How Much Emergency Fund Do You Really Need?

There is no fixed number that works for everyone. The right amount depends on expenses, income stability, and responsibilities.

General Rule of Thumb

Most financial planners recommend keeping 3 to 6 months of essential expenses as an emergency fund.

This is based on expenses, not income.

How to Calculate Your Emergency Fund Correctly

Instead of guessing, calculate it properly using expenses.

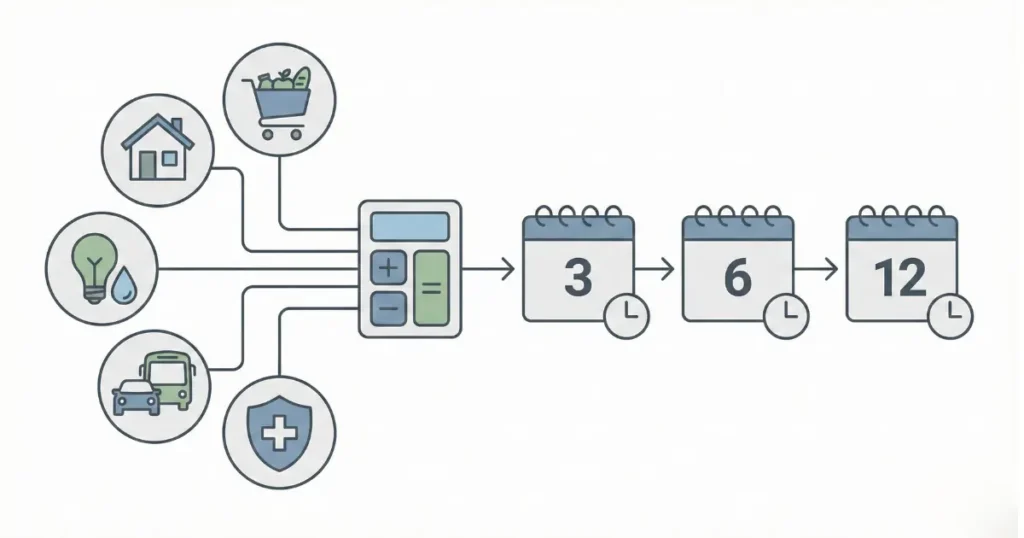

Step 1: List Essential Monthly Expenses

Include only unavoidable expenses such as:

- House rent or home loan EMI

- Groceries and daily essentials

- Electricity, water, internet

- Insurance premiums

- School or basic education costs

- Transportation

- Minimum loan repayments

Exclude:

- Dining out

- Entertainment

- Shopping

- Vacations

- Optional subscriptions

If you’re unsure, the Emergency Fund Calculator on PlanMyReturns helps you separate essential and non-essential expenses and gives you a clear target amount.

Step 2: Choose the Right Coverage Period

Select the number of months based on your situation:

- 3 months: Stable salaried job, dual income household

- 6 months: Single income, dependents, moderate job risk

- 9 to 12 months: Freelancers, business owners, variable income

Example

If your essential monthly expenses are ₹40,000:

- 3 months = ₹1.2 lakh

- 6 months = ₹2.4 lakhs

- 9 months = ₹3.6 lakhs

This is your recommended emergency fund range.

Who Needs a Larger Emergency Fund?

You should maintain a higher emergency buffer if:

- You are self-employed or freelance

- Your income is commission-based or seasonal

- You support parents or dependents

- You have ongoing loan EMIs

- You work in a volatile or high-risk industry

In these cases, relying on just 3 months of expenses can be risky.

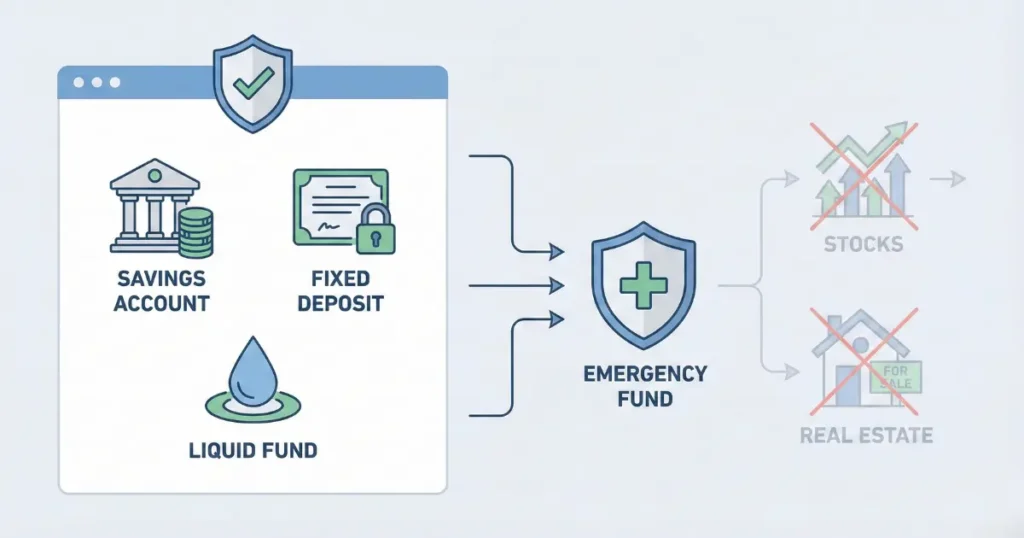

Where Should You Keep Your Emergency Fund?

Emergency funds must be safe, liquid, and easy to access. Returns are secondary.

Best Options to Park Emergency Funds

- High-interest savings accounts

- Sweep-in or auto-fixed deposit accounts

- Short-term liquid mutual funds

- Overnight or ultra-short duration funds

Where You Should Not Keep Emergency Funds

- Equity mutual funds

- Stocks

- ULIPs

- Long-term fixed deposits with penalties

- Real estate or gold

If accessing your money takes more than one working day or involves market risk, it’s not suitable for emergencies.

Emergency Fund vs Fixed Deposit vs Liquid Fund

Each option serves a different purpose:

- Savings account: Instant access, lowest risk

- Fixed deposit: Slightly better returns, limited liquidity

- Liquid fund: Better tax efficiency for larger amounts, usually T+1 access

Many people split their emergency fund between savings and liquid funds for flexibility.

How Long Does It Take to Build an Emergency Fund?

It depends on your monthly surplus.

A practical approach:

- Pause aggressive investing temporarily

- Save a fixed amount every month

- Use bonuses, incentives, or tax refunds to speed up the process

Once your emergency fund is complete, redirect that same monthly amount toward SIPs or other investments.

Common Emergency Fund Mistakes to Avoid

- Investing emergency money in equity for higher returns

- Mixing emergency funds with goal-based savings

- Underestimating actual monthly expenses

- Using emergency funds for lifestyle spending

- Not replenishing the fund after using it

An emergency fund should function like financial insurance, not spare cash.

Emergency Fund vs Insurance: Why You Need Both

Insurance and emergency funds serve different roles:

- Insurance covers large, defined risks like hospitalization or death

- Emergency fund covers immediate cash needs and income disruption

Insurance claims can take time. Emergency funds provide instant access.

You need both for complete financial security.

Why Emergency Funds Create Financial Stability

An emergency fund is not about expecting problems. It’s about being prepared.

It gives you:

- Confidence during uncertainty

- Protection for long-term investments

- Freedom to make better financial decisions

- Peace of mind that money issues won’t force bad choices

Before chasing higher returns, make sure your financial foundation is strong.

If you haven’t built an emergency fund yet, calculate your requirement using the Emergency Fund Calculator on PlanMyReturns and start building it today.

Frequently Asked Questions About Emergency Funds

Yes. Insurance does not cover job loss, income gaps, or everyday emergencies.

In most cases, yes. Especially before equity investments.

Only if it prevents high-interest debt or severe financial stress. Rebuild it immediately after.

Review it once a year or after major life changes such as marriage, job change, or new dependents.

There is no universal number. Use an Emergency Fund Calculator to base it on your actual expenses.