A complete step-by-step guide to filing your income tax return for AY 2026-27 as a salaried employee. Covers due dates, ITR-1 vs ITR-2 eligibility, documents you need, the old vs new regime choice, common mistakes, and what to do if you miss the deadline.

Which law applies this season: Even though the Income-tax Act, 2025 took effect from 1 April 2026, your return for AY 2026-27 reports income earned in FY 2025-26, so it is filed entirely under the old Income-tax Act, 1961, using the familiar ITR forms and section numbers. The new Act and its renumbered provisions apply from AY 2027-28 onward.

Filing your ITR is not just a compliance task, it is how you claim back excess TDS, carry forward losses, and build a clean income record for loans and visas. For salaried employees, the process has become considerably simpler with pre-filled data, but a few decisions, like which ITR form and which tax regime, still need your judgment.

This guide walks through the entire process for AY 2026-27: what changed this year, which form applies to you, what documents to keep ready, and how to file correctly and on time.

Quick Answer: Most salaried employees file ITR-1 online through the income tax e-filing portal using pre-filled salary, TDS, and interest data, choose their preferred tax regime, submit, and e-verify using Aadhaar OTP, all before 31 July 2026.

What’s New for AY 2026-27

- ITR-1 now allows two house properties. Salaried individuals with total income up to Rs 50 lakh can file ITR-1 even if they own two house properties, instead of being pushed to ITR-2 for a second property alone.

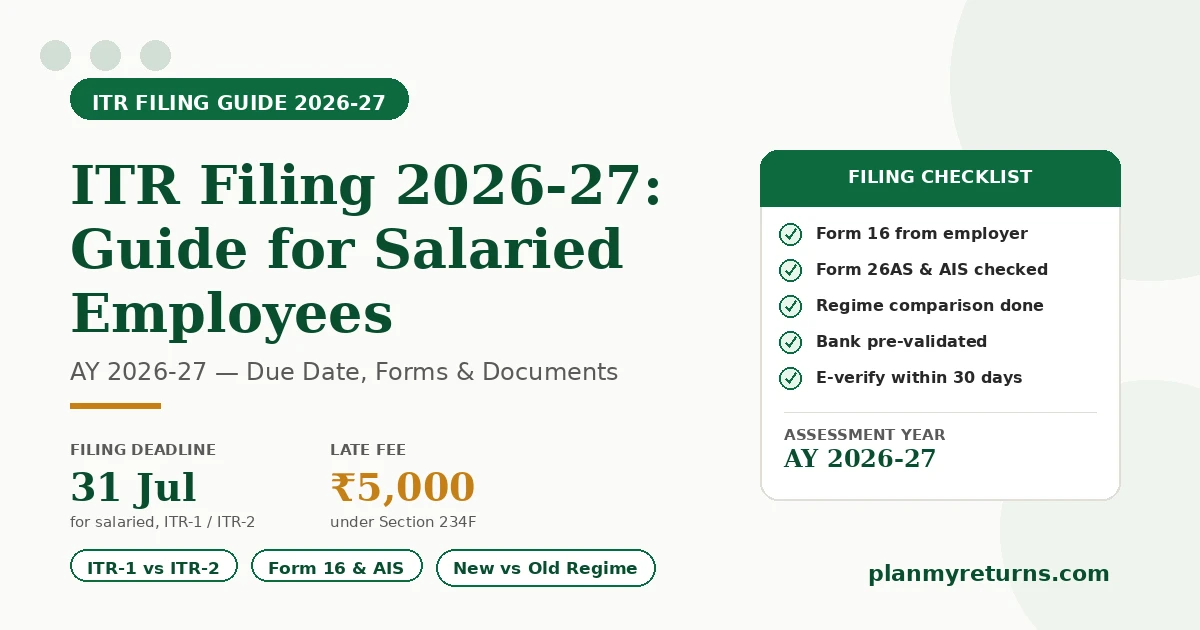

- Staggered due dates. Salaried and other non-audit ITR-1/ITR-2 filers are due 31 July 2026, while non-audit business and professional filers using ITR-3/ITR-4 get an extra month until 31 August 2026.

- New regime slabs continue unchanged. The seven-slab new regime structure and the Rs 60,000 Section 87A rebate introduced in Budget 2025 carry forward without change for FY 2025-26.

- AIS and TIS remain central to pre-fill accuracy. The Annual Information Statement and Taxpayer Information Summary continue to drive most of the pre-filled data in your return, so mismatches here are the most common source of notices.

Who Needs to File ITR-1 vs ITR-2

| Criteria | ITR-1 (Sahaj) | ITR-2 |

|---|---|---|

| Total income | Up to ₹50 lakh | Above ₹50 lakh, or any amount with capital gains |

| Salary or pension income | Yes | Yes |

| House property income | Up to two properties (no carried-forward loss) | Any number of properties |

| Capital gains | Not allowed | Allowed |

| Foreign income or assets | Not allowed | Allowed |

| Agricultural income | Up to ₹5,000 | Above ₹5,000 |

| Director in a company or unlisted shares held | Not allowed | Allowed |

Common trigger for ITR-2: Selling mutual funds, stocks, or property during the year, even a small profit, moves you from ITR-1 to ITR-2, since capital gains cannot be reported in ITR-1 regardless of your total income.

Documents to Keep Ready

- Form 16 from your employer, showing salary, TDS, and deductions considered by payroll

- Form 26AS and the Annual Information Statement (AIS), to cross-check TDS credit and other reported income

- Bank interest certificates for savings accounts and fixed deposits

- Capital gains statements from your broker or mutual fund platform, if applicable

- Home loan interest certificate from your bank, if you are claiming a housing loan deduction

- Rent receipts and the landlord’s PAN, if claiming HRA above the threshold requiring PAN disclosure

- Proof of Section 80C, 80D, and other deductions if you plan to file under the old regime

Step-by-Step Process to File ITR Online

Log In and Select the Assessment Year

Log in to the income tax e-filing portal using your PAN and password. Under the “File Income Tax Return” section, select AY 2026-27, since this reports income earned between April 2025 and March 2026.

Choose the Correct ITR Form

The portal often suggests a form based on your profile, but confirm it against your actual income sources. If you sold any shares, mutual funds, or property during the year, or your income exceeds Rs 50 lakh, choose ITR-2.

Review Pre-Filled Data

The portal pre-fills salary, TDS, interest income, and other details from Form 26AS and AIS. Compare every figure against your Form 16 and bank statements, and correct any mismatch before proceeding, since incorrect pre-filled data does not automatically get fixed.

Choose Your Tax Regime

Confirm whether you want the new regime or the old regime for this return. Salaried individuals without business income can pick either regime independently of what their employer used for TDS during the year, as long as you file by the due date.

Claim Deductions and Compute Tax

If you have chosen the old regime, enter your Section 80C, 80D, HRA, and home loan interest details. The portal computes your total tax liability, adjusts TDS already paid, and shows the refund due or balance tax payable.

Submit and E-Verify

Submit the return and complete e-verification within 30 days, using Aadhaar OTP, net banking, a bank or demat EVC, or a Digital Signature Certificate. An unverified return is treated as not filed, so do not skip this step.

Not sure how much tax you owe before you file? Estimate your liability with your actual salary and deductions.

Try the Income Tax CalculatorCommon Mistakes to Avoid

- Filing under the wrong assessment year, since AY 2026-27 covers FY 2025-26 income, not the current financial year

- Ignoring a mismatch between Form 16 and AIS instead of investigating it before filing

- Choosing ITR-1 despite having capital gains, which makes the return defective

- Forgetting to e-verify after submission, which leaves the return legally unfiled

- Missing bank interest or other income not reflected in Form 16, since AIS usually catches it anyway and triggers a mismatch notice

- Not comparing old versus new regime tax liability before submitting, and defaulting to whichever regime the employer used for TDS

Due Date Calendar for AY 2026-27

*Note: Belated return acceptance and any extension of the original due date can change based on CBDT circulars issued closer to the deadline. Always confirm the current date on the e-filing portal before you rely on it.

Penalty for Late or Missed Filing

Section 234F charges a late filing fee of up to Rs 5,000 if you file after the due date but before 31 December 2026, reduced to Rs 1,000 if your total income is up to Rs 5 lakh. Beyond this, interest under Section 234A accrues on any unpaid tax from the original due date until you file.

Expert Tip: A belated return also restricts you from carrying forward most business or capital losses to future years, even though you can still claim deductions and get your refund. If you expect a loss you want to carry forward, filing on time matters more than the late fee itself.

Decision Checklist Before You File

- Confirm you are filing for AY 2026-27, reporting income earned between April 2025 and March 2026

- Confirm whether ITR-1 or ITR-2 applies, especially if you had any capital gains during the year

- Reconcile Form 16 against Form 26AS and AIS before you start filling the return

- Compute tax under both regimes and pick whichever is lower for your situation

- Confirm your bank account is pre-validated on the portal so any refund is credited without delay

- Complete e-verification within 30 days of submission, since this step is easy to forget

Frequently Asked Questions

Conclusion

Filing ITR for AY 2026-27 still runs on the familiar 1961 Act framework, so if you have filed before, the process itself has not changed dramatically. What has changed is the ITR-1 eligibility for two house properties and the staggered due dates by taxpayer category. Reconcile your documents against AIS, pick the regime that actually costs less, and file well before 31 July to avoid the late fee and loss-carry-forward restrictions.

Before you file, check your numbers with the Income Tax Calculator and compare regimes using the Old vs New Tax Regime Calculator. If you are claiming HRA, the HRA Exemption Calculator can help you verify the exempt amount before you enter it in your return.