Discover how small PPF investments compound into lakhs over time. Complete PPF calculator guide for FY 2026-27 with real scenarios, maturity projections, and step-by-step walkthrough of how to use the PPF calculator.

If you invest just ₹1,000 per month in PPF for 25 years at the current 7.1% interest rate, your tax-free corpus grows to approximately ₹8.25 lakhs. Increase it to ₹5,000/month and you are looking at ₹41.25 lakhs. Go to ₹12,500/month (maxing out the ₹1.5 lakh annual limit) and you cross ₹1 crore in 25 years. Entirely tax-free.

This is the quiet power of PPF compounding. No stock market drama, no market crashes, no tax headaches. Just guaranteed government-backed interest working silently in the background for 15 to 25 years.

In this guide, we show you exactly how PPF compounds, how to use the PPF calculator to project your corpus, and the one trick that can add lakhs to your final amount. All calculations are based on the current 7.1% PPF rate for FY 2026-27.

How Much Does ₹1,000/Month in PPF Actually Become?

Let us start with the headline number everyone wants to see. Here is how ₹1,000 per month (₹12,000/year) in PPF grows at 7.1% annual interest:

Notice the pattern? In 15 years, your interest (₹1.45 lakh) roughly matches your investment (₹1.8 lakh). But stretch the account to 25 years (using two 5-year extensions), and your interest earned (₹5.24 lakh) is nearly 1.75x your total investment. That is the magic of compound interest.

The earlier 5,000/month or 12,500/month figures from our intro? Just multiply these numbers. Use the PlanMyReturns PPF Calculator to run your exact monthly amount.

What will YOUR monthly PPF amount grow to?

Get year-by-year projections with our free PPF calculator.

PPF Calculator Formula: How Interest Is Calculated

PPF uses standard compound interest formula with annual compounding. Here is the exact math your PPF calculator runs behind the scenes:

P = Annual PPF deposit

r = Annual interest rate (7.1% = 0.071)

n = Number of years

This is the formula for annuity-due compounding (deposits made at the start of each year). If you deposit lump sum on April 1 every year, this formula gives you the exact maturity amount.

One crucial rule about PPF interest calculation: Interest is computed on the lowest balance between the 5th and end of each month, then credited annually on March 31. This single rule can make or break your final PPF corpus.

The ₹1-Lakh Trick: Deposit your PPF contribution before April 5th every year (not spread across the year). A ₹1.5 lakh/year investor who deposits on April 1 earns roughly ₹1 lakh more over 15 years than someone who deposits on March 31 of each year. Same amount, same scheme. Just better timing.

How to Use the PPF Calculator on PlanMyReturns

Using our PPF Calculator takes under 30 seconds. Here is the step-by-step walkthrough:

Enter Your Monthly or Yearly Investment

Start with what you can realistically commit. Common amounts: ₹1,000, ₹2,500, ₹5,000, ₹10,000, ₹12,500 per month. The calculator accepts both monthly and annual inputs. Keep in mind the cap is ₹1,50,000 per financial year (₹12,500/month maximum).

Choose Your Investment Tenure

Default is 15 years (the minimum lock-in). But you can extend PPF in 5-year blocks after maturity. Select 15, 20, 25, or 30 years to see the dramatic difference compounding makes over longer periods.

Confirm the Interest Rate

The calculator auto-fills the current rate (7.1% for FY 2026-27). You can also manually change it to run “what if” scenarios. Historically, PPF rates have ranged from 7.1% to 8.7% over the last decade. The government revises the rate every quarter.

View Results and Year-by-Year Breakdown

Hit calculate. You get three key numbers: total investment, total interest earned, and final maturity amount. Scroll down for the year-by-year schedule showing exactly how your balance grows each year. This makes compounding visible and motivating.

Compare Scenarios

Run the calculator 2-3 times with different inputs. Try ₹5,000 vs ₹10,000 monthly. Try 15 years vs 25 years. Try 6.9% vs 7.5% interest rates. Seeing the gap helps you decide how much to invest and whether to extend your PPF account after 15 years.

PPF Growth Scenarios: Find Yours

Here are the most common PPF investment amounts and their maturity values at 7.1% over 15 years. Find the scenario closest to yours:

Maxing out PPF = ₹40.68 lakh tax-free in 15 years. Extend it for 2 more 5-year blocks and the same ₹12,500/month investment crosses ₹1 crore. That is the magic of EEE status combined with 25-year compounding.

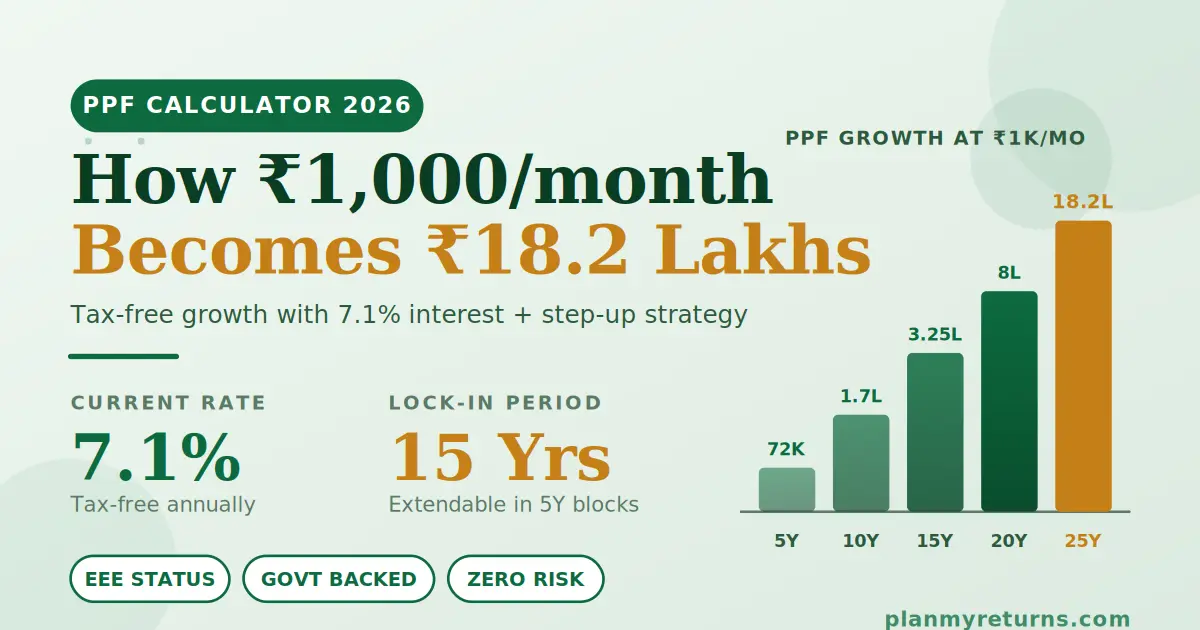

The ₹1,000/Month Trick That Becomes ₹18.2 Lakhs

The title of this post claims ₹1,000/month becomes ₹18.2 lakhs. Here is how that actually works. It is not straight 25-year compounding. It is a smarter approach we call the Step-Up PPF strategy.

Instead of keeping your PPF contribution flat at ₹1,000/month forever, you increase it by 10% every year as your salary grows. Here is the real math:

Starting small at ₹1,000/month and growing your PPF contribution 10% every year (in line with typical salary hikes) builds a tax-free corpus of approximately ₹18.2 lakhs in 25 years. You never feel the pinch because each year’s increase is only marginally more than the last.

For context, the exact same ₹18.2 lakhs corpus would require you to save ₹1,820/month flat for 25 years. The step-up approach starts 45% lower and catches up naturally.

PPF Interest Rate History: What to Expect

PPF interest rates are reviewed every quarter by the Ministry of Finance. Here is the recent history to help you understand the range:

PPF has held steady at 7.1% since Q2 FY 2020-21. This is the longest stable period in PPF history. Rates do adjust every quarter based on government securities yields, so your actual returns may vary. The PPF Calculator auto-updates to the latest rate.

5 Smart PPF Strategies Most Indians Miss

Strategy 1: Always deposit before April 5th. Interest is calculated on the minimum balance between the 5th and end of each month. A ₹1.5 lakh deposit on April 1 earns 11 months of interest in that year. The same deposit on April 10 earns only 11 months on the portion, but you lose roughly 0.6% interest for that first month. Over 15 years, this timing difference alone adds up to ₹80,000+.

Strategy 2: Open a PPF account early for your child. A PPF account in your minor child’s name (with you as guardian) lets you invest up to ₹1.5 lakh from birth. By the time they turn 18, the account has compounded for 18 years. At ₹1,000/month, that is approximately ₹4.6 lakh completely tax-free. Perfect for higher education.

Strategy 3: Extend indefinitely after 15 years. After maturity, you have 3 options: withdraw, extend with contributions (submit Form H), or extend without contributions. The “extend without contributions” option is underrated. Your existing balance keeps earning tax-free interest, but you can still make one withdrawal per financial year. Great for retirement income planning.

Strategy 4: Use PPF as your debt allocation. If your portfolio target is 70% equity (ELSS, mutual funds) and 30% debt, PPF is the best debt instrument available for tax efficiency. It beats FDs and debt mutual funds on post-tax returns for the 20% and 30% slab. Use the Asset Allocation Calculator to find your ideal mix.

Strategy 5: Avoid premature withdrawal. Partial withdrawals are allowed from the 7th year onwards, but every rupee withdrawn loses its compounding power for the remaining tenure. A ₹50,000 withdrawal in year 8 costs you approximately ₹85,000 in lost interest over the remaining 7 years. Treat PPF as truly untouchable unless there is a genuine emergency.

Run YOUR exact PPF scenario now.

Annual or monthly deposits, year-by-year breakdown, instant maturity projection.

Real-Life Example: Arjun’s PPF Journey

Arjun, 28, HR Executive in Pune. Monthly salary: ₹55,000. Goal: ₹50 lakh corpus by age 48.

Arjun opened his PPF account in April 2026 and committed to ₹5,000/month (₹60,000/year). Using the PPF calculator, here is how his plan plays out:

Phase 1 (Years 1-15): Flat ₹5,000/month. At 7.1%, his year 15 balance = ₹16.27 lakh. Total invested: ₹9 lakh. Tax-free interest earned: ₹7.27 lakh.

Phase 2 (Years 16-20): First 5-year extension with contributions. Arjun increases to ₹10,000/month as his salary grew. Year 20 balance crosses ₹35 lakh.

Phase 3 (Years 21-25): Second 5-year extension with max ₹12,500/month contribution. Year 25 balance: ₹54.8 lakh. Completely tax-free.

Simultaneously, Arjun runs a ₹10,000/month ELSS SIP (80C-eligible) for market-linked growth. His combined tax-saving portfolio achieves the ₹1.5 lakh 80C cap while balancing safety (PPF) and growth (ELSS). Plan a similar combo using the SIP Calculator alongside the PPF calculator.

PPF vs Other Tax-Saving Options

PPF is one of the best 80C instruments, but not the only one. Here is how it compares to popular alternatives:

For risk-averse investors in the 30% tax bracket, PPF beats FDs and NSC on post-tax returns by a wide margin. A 7.1% tax-free PPF return is equivalent to a 10.15% pre-tax FD return. No bank offers that. Compare exact numbers using the FD Calculator.

Plan Your Complete Savings Portfolio

PPF is the anchor of any tax-efficient portfolio, but it should not be your only investment. Combine it with these complementary options on PlanMyReturns.

Build equity exposure through monthly SIPs using the SIP Calculator. If you have a daughter, pair PPF with Sukanya Samriddhi (SSY Calculator) for even better 8.2% returns. Maximize your 80C by adding NPS for the extra ₹50,000 deduction via the NPS Calculator. Plan your retirement corpus target with the Retirement Calculator. And track your crorepati milestone using the Crorepati Calculator.

Explore all free financial calculators at PlanMyReturns Calculators. Every calculation follows transparent methodology and assumptions.

Frequently Asked Questions: PPF Calculator