A complete guide to Step-Up SIP for Indian investors. See how a 10% annual increase in your monthly SIP nearly doubles your final corpus over 25 years, why it beats regular SIP for salaried professionals, and how to set it up automatically.

A Step-Up SIP is a Systematic Investment Plan where you increase your monthly investment by a fixed percentage every year, typically matching your annual salary hike. It is one of the most powerful wealth-building strategies available to Indian salaried investors, yet less than 15% of SIP investors use it.

Why? Because most people set up their SIP once and forget it. They invest ₹10,000/month in year 1, and they are still investing ₹10,000/month a decade later, even though their salary has tripled. This is a massive missed opportunity.

In this guide, you will see exactly how Step-Up SIP works, the math behind why it nearly doubles your wealth, and how to start one in 5 minutes.

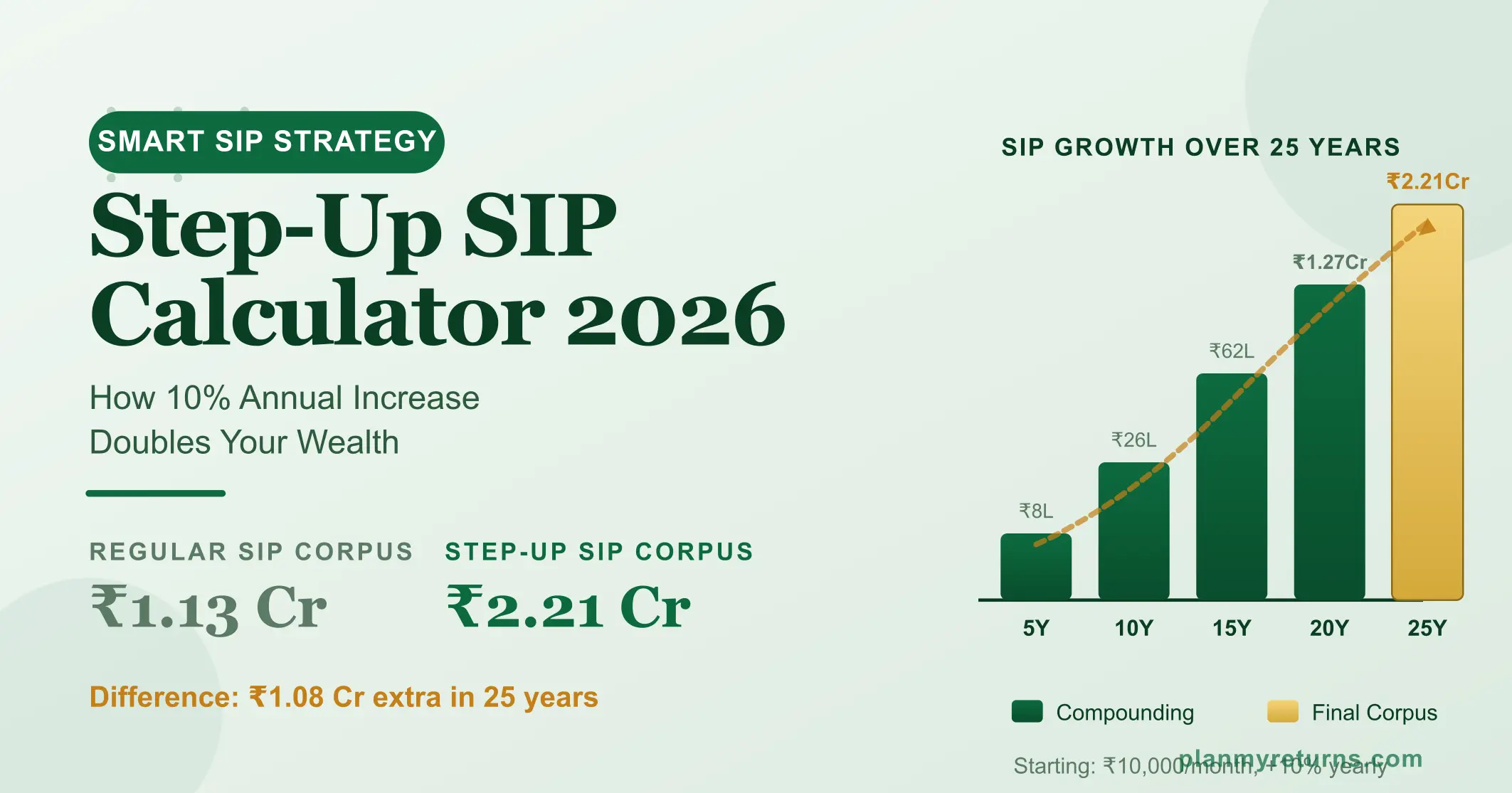

Real numbers ahead. A regular ₹10,000 monthly SIP at 12% returns grows to ₹1.13 crore in 25 years. A 10% step-up SIP starting at ₹10,000 grows to ₹2.21 crore. That is ₹1.08 crore extra, just by stepping up your SIP every year.

What is a Step-Up SIP?

A Step-Up SIP is a regular Systematic Investment Plan where the monthly investment amount increases by a pre-set percentage on a fixed date every year. Most platforms let you choose the step-up percentage (5%, 10%, 15%, or any custom value) and the frequency (annual is most common).

Here is what a 10% annual step-up SIP looks like in practice, starting with ₹10,000/month:

Notice how the monthly SIP grows naturally with your income. This is the key idea: your investments should grow at the same pace as your salary, not stay frozen at year-1 levels.

Step-Up SIP vs Regular SIP: The Real Difference

Let us compare both side by side. Same starting amount (₹10,000/month), same expected return (12% per annum), same duration (25 years).

The difference: ₹1.08 crore extra in your bank. Almost double the corpus, just for incrementally increasing your SIP each year. And it gets even better at higher step-up rates.

See your exact step-up SIP corpus instantly.

Try different step-up percentages and durations.

Why Step-Up SIP Works: The Math Behind the Magic

Step-Up SIP works because of two powerful forces working together: compounding and increasing contributions. Let us break it down.

Force 1: Compounding on more money. A regular SIP compounds the same ₹10,000/month for 25 years. A step-up SIP compounds increasing amounts. By year 25, you are investing ₹98,497/month, all earning 12% returns. The later contributions are larger, so the absolute compounding is larger.

Force 2: Salary inflation match. Your salary grows 8 to 12% per year on average in India. Step-Up SIP ensures your investments grow at the same pace. Without step-up, your savings rate as a percentage of income drops every year, even though you are getting raises.

The real secret: it does not feel painful. Increasing your SIP from ₹10,000 to ₹11,000 after a salary hike feels like nothing. You barely notice it. But over 25 years, those small annual nudges compound into a life-changing difference.

How to Start a Step-Up SIP in 5 Minutes

Calculate Your Target Corpus

Decide what you are saving for. Retirement at 60? Child’s education at 18? A house in 15 years? Each goal needs a target corpus. For example, ₹5 crore for retirement at 60. Use the Retirement Calculator or Education Planning Calculator to find your number.

Reverse-Engineer the SIP Amount

Open the SIP Calculator and enter your target corpus, expected return (12% for equity), and duration. The calculator will show you the monthly SIP needed. If the number feels too high, lower your starting amount and increase the step-up percentage. A 15% step-up requires a smaller starting SIP than a flat investment.

Choose the Right Mutual Fund

For long-term goals (10+ years), pick equity mutual funds like Nifty 50 index funds, large cap funds, or flexicap funds. For medium-term goals (5-10 years), consider balanced advantage funds. Avoid debt funds for step-up SIPs as they typically deliver 6 to 7% returns, not enough to outpace inflation.

Register the Step-Up on Your Platform

Major platforms like Groww, Zerodha Coin, Kuvera, Paytm Money, ET Money, and most AMC websites support automatic Step-Up SIP. When registering the SIP, look for “Step-Up SIP” or “Top-Up SIP” option. Set the percentage (10% recommended) and the step-up date (your salary hike month works best).

Automate and Forget

Once registered, the platform automatically increases your SIP every year on the chosen date. You do not have to log in or do anything. Just review once a year. If your salary grew faster than 10%, you can manually bump up the step-up rate. If you switched jobs and income jumped 30%, increase your SIP by 25-30% one-time.

How big can your step-up SIP grow?

Calculate corpus for any starting amount and step-up percentage.

Step-Up SIP for Different Goals

Step-Up SIP shines when applied to specific financial goals. Here is how to use it for the three biggest life goals Indians plan for:

Goal 1: Retirement Planning

If you are 30 years old and want ₹5 crore at age 60, a regular flat SIP at 12% return needs ₹16,500/month for 30 years. A 10% step-up SIP needs only ₹6,500 starting amount. Most 30-year-olds can spare ₹6,500/month easily, while ₹16,500/month feels like a stretch. Use the Retirement Calculator to find your retirement corpus.

Goal 2: Child’s Higher Education

An MBA from a top Indian college costs ₹25 lakh today. With 8% education inflation, it will cost ₹1.16 crore in 18 years. A 10% step-up SIP starting at ₹4,500/month will get you there. A flat SIP needs ₹15,000/month from day one. Use the Education Planning Calculator to plan for your child.

Goal 3: Buying a Home

If you want a ₹80 lakh down payment in 12 years, a 10% step-up SIP starting at ₹15,000/month gets you there at 12% returns. The Dream Home Calculator on PlanMyReturns shows you the exact monthly investment needed for any home buying goal.

Common Step-Up SIP Mistakes to Avoid

Mistake 1: Setting step-up percentage too low. A 5% step-up barely beats inflation. If you are getting 10% salary hikes but only stepping up 5%, you are leaving money on the table. Match your step-up rate to your salary growth.

Mistake 2: Starting too late. Starting a step-up SIP at age 40 instead of 25 cuts your final corpus by more than half. Compounding needs time. Start the smallest possible step-up SIP today, even ₹500/month, rather than waiting for “the right amount.”

Mistake 3: Stopping during market crashes. The biggest wealth destroyer is panic-stopping your SIP during market falls. Step-up SIPs work because they buy more units when markets are down. Stay invested. Better yet, increase your step-up during prolonged bear markets.

Mistake 4: Not increasing step-up after big salary jumps. If you got a 40% raise from a job switch, do not just continue with 10% step-up. Bump your SIP up immediately by 25-30% to match your new income reality.

Mistake 5: Choosing wrong fund category. A step-up SIP in a debt fund or hybrid fund will not beat inflation over 25 years. For long-term goals, equity is essential. For tax saving + step-up, use the ELSS Calculator to plan your equity-linked savings.

Real-Life Example: Rahul’s Crorepati Journey

Rahul, 28, Marketing Manager in Pune. Annual salary: ₹12,00,000. Target: ₹3 crore by age 50.

Rahul has 22 years until his target. A flat SIP needs ₹19,000/month at 12% returns to reach ₹3 crore. That is 19% of his current monthly take-home, which feels too aggressive.

Instead, Rahul opts for a 10% step-up SIP starting at ₹8,500/month. That is just 8.5% of his current take-home, completely manageable. By year 22, he will be investing ₹68,000/month, but his salary will likely be ₹40 lakh+ per year by then, making it a small percentage.

Result: Rahul ends up with ₹3.04 crore at age 50, having invested a total of ₹68 lakh over 22 years. The remaining ₹2.36 crore is pure compounding magic. Use the Crorepati Calculator to plan your own journey to ₹1 crore or more.

Want to retire as a crorepati?

See how much step-up SIP you need to reach any wealth target.

Step-Up SIP vs Other Investment Strategies

Compare exact returns yourself: SIP Calculator vs Lumpsum Calculator vs FD Calculator.

Plan Your Complete Financial Journey

A step-up SIP is the engine of long-term wealth creation, but you also need other building blocks. Use these calculators on PlanMyReturns to complete your financial plan.

Calculate exact tax savings on equity gains using the Capital Gains Calculator. If you are starting an SWP after retirement, plan it with the SWP Calculator. Build your asset allocation strategy with the Asset Allocation Calculator. And to retire early on your terms, check the FIRE Calculator.

Explore all free financial calculators at PlanMyReturns Calculators. Every calculation follows transparent methodology and assumptions you can verify.

Frequently Asked Questions: Step-Up SIP