The top ELSS mutual funds in India for 2026 based on 3-year and 5-year rolling returns, expense ratio, fund size, and risk-adjusted performance. Plus, how to pick the right ELSS fund for your goals and start a tax-saving SIP.

ELSS (Equity Linked Savings Scheme) is the only mutual fund category that qualifies for Section 80C tax deduction up to ₹1,50,000 per year. With just a 3-year lock-in and historical returns of 12-15% CAGR, ELSS beats every other 80C instrument for wealth creation. But with 40+ ELSS funds in the market, picking the right one matters more than picking any fund.

We have analyzed every ELSS fund in India based on 3-year rolling returns, 5-year rolling returns, expense ratio, fund manager consistency, portfolio quality, and risk-adjusted performance (Sharpe ratio). Here are the top 5 ELSS mutual funds to invest in through SIP for 2026, ranked by overall performance.

Important: Past performance does not guarantee future returns. This analysis is for educational purposes. Use the ELSS Calculator to estimate your own returns based on your investment amount and tenure.

How We Ranked the Top ELSS Funds for 2026

Our ranking methodology looks at what actually matters for long-term SIP investors, not just last year’s hot performer. Here are the 5 parameters we weighted:

All return data is as of March 31, 2026. Expense ratios are for direct plans only, since direct plans save 0.5-1% annually compared to regular plans. Always invest through direct plans on platforms like MF Central, AMC websites, or Groww/Zerodha (direct mode).

Top 5 Best ELSS Mutual Funds for 2026

1. Quant ELSS Tax Saver Fund (Direct)

Best for aggressive investors seeking alpha generation

Why it ranks #1: Quant ELSS has consistently topped ELSS category returns for the past 3 years. The fund follows a VLRT (Valuation, Liquidity, Risk, Time) framework that actively rotates between sectors based on market cycles. Under fund manager Sandeep Tandon, the scheme has generated the highest alpha in the ELSS category.

Best for: Investors under 35 with 7+ year horizon and high risk tolerance. Not suitable if you get nervous during 20-30% drawdowns.

2. Mirae Asset ELSS Tax Saver Fund (Direct)

Best all-rounder for first-time ELSS investors

Why it ranks #2: Mirae Asset ELSS Tax Saver is the most consistent performer in the ELSS category over the last 10 years. The fund follows a Growth at Reasonable Price (GARP) approach and maintains a large-cap heavy portfolio (60-65%) with quality mid-caps. One of the lowest expense ratios in the category makes it extremely cost-efficient.

Best for: First-time ELSS investors, anyone wanting a core portfolio holding, those preferring stability over aggressive returns. Ideal starting fund for SIP of ₹5,000-₹12,500 per month.

3. Parag Parikh ELSS Tax Saver Fund (Direct)

Best for value-oriented, long-term investors

Why it ranks #3: PPFAS Mutual Fund is known for its value investing philosophy and transparent communication. The ELSS Tax Saver fund follows the same principles, focusing on quality businesses at reasonable valuations. Unlike their flagship Flexi Cap fund, this one invests only in Indian equities (SEBI rule for ELSS). Excellent downside protection during market corrections.

Best for: Long-term investors with 10+ year horizon, those who value capital protection alongside growth, investors aligned with value investing philosophy.

4. SBI Long Term Equity Fund (Direct)

Best for conservative ELSS investors preferring largecap bias

Why it ranks #4: SBI Long Term Equity Fund (formerly SBI Magnum Tax Gain) is India’s oldest ELSS scheme, launched in 1993. With over 30 years of track record, it has weathered multiple market cycles. The fund follows a blend of value and growth investing with a large-cap bias. Strong performance turnaround in the last 3 years under fund manager Dinesh Balachandran.

Best for: Conservative investors who want ELSS exposure with large-cap bias, those preferring established AMCs, investors who value long track record over recent stars.

5. Canara Robeco ELSS Tax Saver Fund (Direct)

Best for risk-averse investors seeking downside protection

Why it ranks #5: Canara Robeco ELSS has built a reputation for strong downside protection during market falls. During the 2020 COVID crash and 2022-23 correction, this fund fell significantly less than category average. The fund maintains a quality-focused portfolio with emphasis on businesses with strong competitive moats and predictable earnings.

Best for: Risk-averse investors who prioritize capital protection, those nearing the end of their equity investing years, investors who cannot tolerate large drawdowns.

Quick Comparison: Top 5 ELSS Funds 2026

Here is a side-by-side comparison of all 5 top ELSS funds. Use this to match the fund to your investor profile.

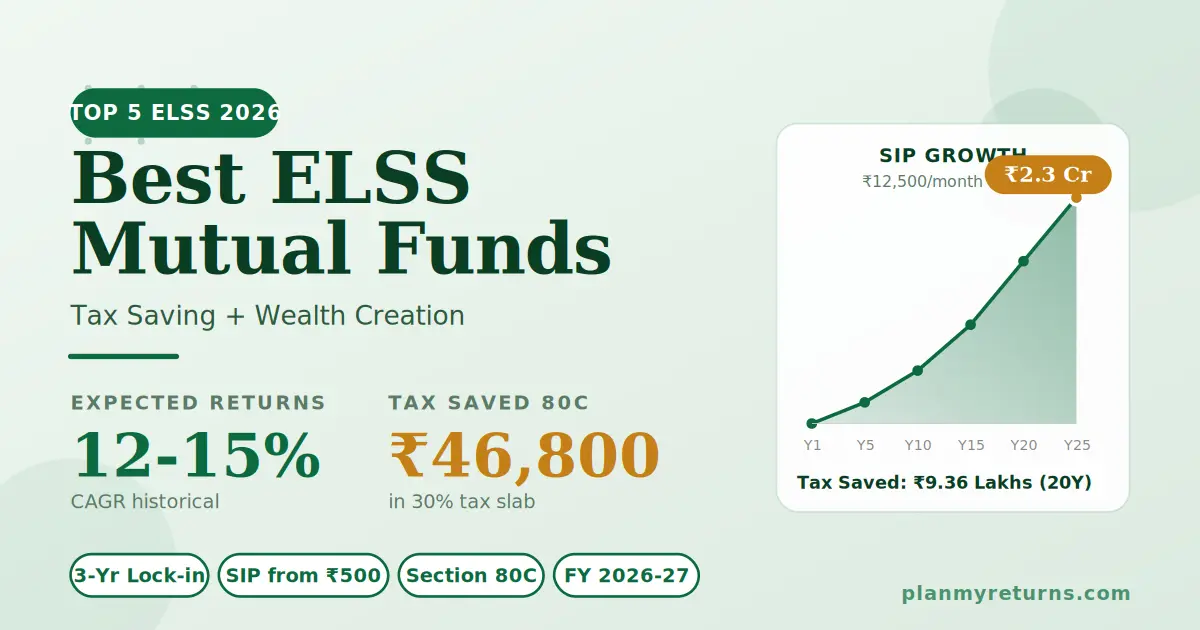

How Much Tax Can You Save with ELSS SIP?

Let us run the math on real SIP amounts. Assuming 12% annualized return (conservative ELSS estimate) and 30% tax bracket:

The ₹12,500 monthly SIP is the sweet spot. It exactly exhausts your ₹1.5 lakh 80C limit while avoiding lumpsum timing risk. Over 20 years, this single habit can build a ₹1.25 crore corpus plus save ₹9.36 lakhs in cumulative tax (₹46,800 × 20 years).

Calculate your exact ELSS returns and tax savings.

Enter your SIP amount, tenure, and tax slab to see your potential corpus.

How to Pick the Right ELSS Fund for You

Do not just pick the top-ranked fund. Match it to your profile. Here is a simple decision framework:

If you are under 30 with high risk tolerance: Go with Quant ELSS Tax Saver for maximum growth potential. The volatility does not matter over 20+ years if you keep investing through market cycles.

If this is your first ELSS investment: Start with Mirae Asset ELSS Tax Saver. It is the safest bet for a beginner with consistent performance, low expense ratio, and large stable fund size.

If you believe in value investing: Parag Parikh ELSS Tax Saver aligns with the long-term value philosophy. Great downside protection during corrections.

If you want largecap bias: SBI Long Term Equity Fund is built for you. 60%+ largecap allocation means less volatility and steadier returns.

If you cannot stomach volatility: Canara Robeco ELSS provides the best downside protection. Your returns will be lower but your nerves will thank you.

Pro tip on diversification: You can split your ₹12,500 monthly SIP across 2 ELSS funds (e.g., ₹6,250 each in Mirae Asset and Parag Parikh). This diversifies fund manager risk without adding complexity. Avoid splitting across more than 2 funds. It dilutes returns.

Common ELSS Mistakes to Avoid

Mistake 1: Investing lumpsum in March. Last-minute lumpsum ELSS investment in March is risky. If markets are at peak, you lock in at the top. Start a monthly SIP from April to spread investments across 12 months and average out volatility.

Mistake 2: Chasing last year’s top performer. The #1 ELSS fund of 2024 is rarely the #1 of 2026. Quant ELSS had back-to-back winning years, but this is exceptional. Look at 5-year rolling returns, not 1-year toppers.

Mistake 3: Investing in regular plans via advisors. Regular plans charge 0.75-1% higher expense ratio than direct plans. Over 20 years, this compounds to ₹15-20 lakhs lost on a ₹12,500 monthly SIP. Always pick direct plans on MF Central, Groww, Kuvera, or AMC websites.

Mistake 4: Redeeming right after 3 years. ELSS is not a 3-year product. It is a wealth creation vehicle with a 3-year minimum. The real compounding magic happens between years 5-20. Keep your ELSS units even after lock-in ends.

Mistake 5: Over-diversifying across 5+ ELSS funds. Owning 5 different ELSS funds gives you returns equal to the category average (which is lower than any top fund). Stick to 1-2 quality funds and let them compound.

How to Start ELSS SIP in 2026 (Step by Step)

Step 1: Complete KYC if not done. You need PAN, Aadhaar, and a cancelled cheque. Online KYC takes 10 minutes via CAMS, KFintech, or MF Central.

Step 2: Pick your ELSS fund from the top 5 list above based on your profile.

Step 3: Choose a direct plan platform. Options include MF Central (free, official), Groww, Zerodha Coin, Kuvera, or the AMC website directly. Avoid regular plans on bank apps.

Step 4: Decide your SIP amount. For full 80C exhaustion: ₹12,500/month. For partial: ₹5,000-₹10,000/month.

Step 5: Set up auto-debit (NACH mandate) on your bank account. Pick a date like 5th or 10th of every month, right after salary credit.

Step 6: Save your investment proofs (ELSS account statement) for income tax filing. Upload them to the tax portal under Section 80C.

See your corpus and tax savings before investing.

Plug in your SIP amount and tenure to see projected wealth.

ELSS vs Other 80C Options: Quick Comparison

Not sure if ELSS is the right choice for your tax saving? Here is how it compares to other popular Section 80C options:

ELSS wins on returns potential and liquidity (shortest lock-in). PPF wins on guaranteed returns and tax-free maturity. The smart move is to split your ₹1.5 lakh across both. Read our complete guide on Section 80C investments for allocation strategies.

Plan Your Complete Financial Journey

ELSS is one part of your tax and wealth plan. Complete the picture with these calculators on PlanMyReturns.

Compare old vs new tax regime using the Income Tax Calculator. Plan your PPF corpus over 15 years with the PPF Calculator. Estimate capital gains tax on your ELSS redemptions using the Capital Gains Calculator. Build your retirement corpus estimate with the Retirement Calculator. Or become a crorepati with systematic investing using the Crorepati Calculator.

Explore all free financial calculators at PlanMyReturns Calculators. Every calculation follows transparent methodology and assumptions you can verify.

Frequently Asked Questions: ELSS Mutual Funds 2026