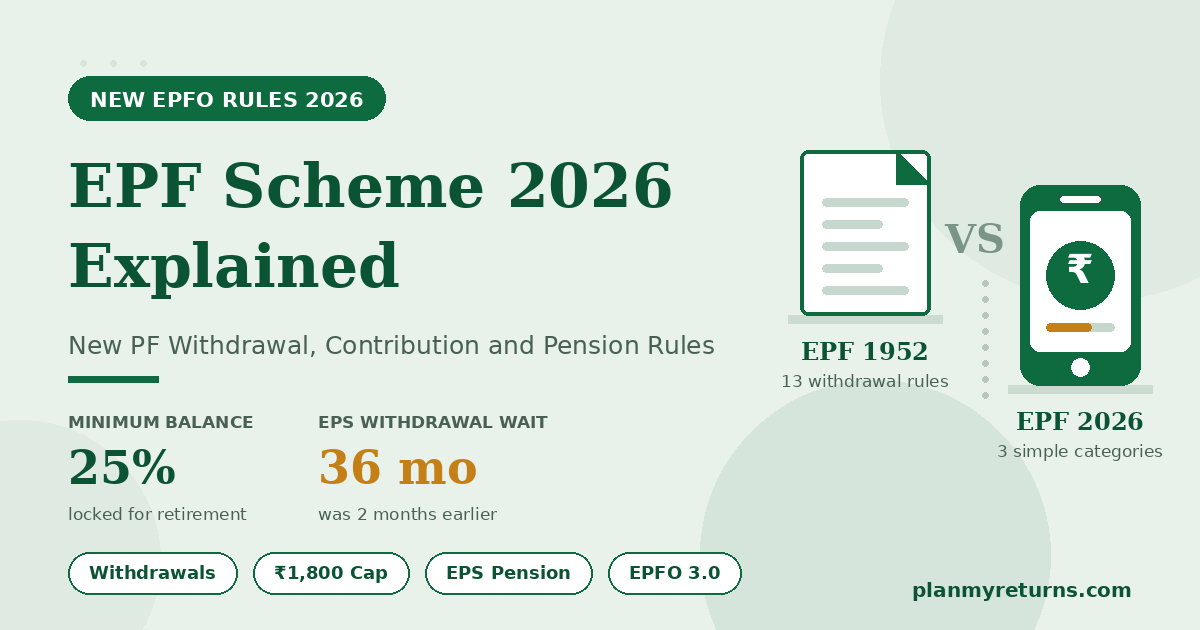

A complete guide to the EPF Scheme 2026, the biggest overhaul of India’s provident fund system since 1952. Understand the new PF withdrawal rules, the 25% minimum balance requirement, the Rs 1,800 mandatory contribution clarification, EPS pension changes, and what every salaried employee should do now.

The Government of India has notified the Employees’ Provident Fund Scheme, 2026, replacing the 74-year-old EPF Scheme, 1952 with effect from June 29, 2026. The new framework operates under the Code on Social Security, 2020 and changes how nearly 8 crore active EPFO members withdraw, contribute, and plan their retirement money.

For most salaried Indians, PF is the single largest forced saving they will ever build. The 2026 rules make withdrawals simpler and more generous, but they also lock 25% of your corpus permanently for retirement and delay pension withdrawals by three years. This guide explains every change with real numbers and what you should actually do.

One thing first: your existing PF balance, UAN, and membership continue automatically. No re-enrolment. No new account. No action needed on the account itself.

Note: These rules took effect days ago and operational circulars are still being issued. Always verify specifics on the official EPFO website (epfindia.gov.in) or with your employer before filing a claim. Want to project your corpus under the new rules? Use the EPF Calculator.

What Is the EPF Scheme 2026?

The EPF Scheme, 2026 is the new legal framework governing provident fund accounts in India. It was notified by the Ministry of Labour and Employment and published in the Gazette, taking effect on June 29, 2026. Alongside it, the government also notified the Employees’ Pension Scheme, 2026, replacing the older EPS framework.

The change is part of implementing the Code on Social Security, 2020, one of India’s four consolidated labour codes. The stated goals are simpler withdrawals, stronger digital compliance, better account portability, and modernised administration through the cloud-based EPFO 3.0 platform.

What Has Not Changed

Early coverage created confusion, so here is what stays exactly the same. The contribution rate remains 12% of wages each for employee and employer, with 10% for certain notified establishments. The pension formula is unchanged: pensionable salary multiplied by pensionable service, divided by 70. The minimum pension stays at ₹1,000 per month. Your UAN, balances, and past contributions carry forward untouched.

The ₹1,800 Contribution Clarification

One widely discussed provision clarifies the split between compulsory and voluntary contributions. The 12% PF contribution is compulsory only up to the statutory wage ceiling of ₹15,000 per month. That caps the mandatory contribution at ₹1,800 per month each for employee and employer, regardless of actual salary.

An employee earning ₹1 lakh basic per month is still legally required to contribute only ₹1,800. Anything above that is now clearly voluntary. Employers may match the voluntary portion but are not required to, and both sides can reduce or stop the extra amount later.

Important: This is a legal clarification, not a cut in your PF. Many employers already contribute on full basic salary as a matter of contract or practice. Whether your in-hand salary changes depends entirely on your employer’s structure. Check with HR before assuming anything.

New Withdrawal Rules: 13 Provisions Become 3 Categories

The old scheme had 13 separate purpose-wise withdrawal provisions, each with its own conditions. Members found the maze confusing. The 2026 scheme merges everything into three categories, all available after just 12 months of membership.

Essential Needs: Illness, Education, Marriage

For illness of self or family, you can withdraw up to 100% of your eligible balance. Education withdrawals for self or family are allowed up to 10 times during membership. Marriage withdrawals are allowed up to 5 times.

Context: The old rules allowed a combined limit of only 3 withdrawals for education and marriage together. The new limits of 10 and 5 are a substantial expansion.

Housing Needs: Purchase, Construction, Loan Repayment

Covers buying, constructing, or renovating a house, and repaying a home loan. Reported limits allow up to 75% of the total balance after 12 months, with a maximum of 5 withdrawals.

Tip: If you plan to use PF for a home purchase, compare the cost of withdrawing PF against extra borrowing. Run the numbers on the Home Loan EMI Calculator and the Buy vs Rent Calculator first.

Special Circumstances: Calamities and Emergencies

Covers natural calamities and other specified emergencies or financial stress. A notable relaxation: withdrawals under special circumstances do not require any additional explanation or documentation of reason.

The 25% Minimum Balance Rule Explained

This is the trade-off for easier access. Members must always retain at least 25% of total accumulated contributions in the EPF account when making partial withdrawals. So when headlines say “withdraw up to 100% of eligible balance,” the word eligible is doing the work. Your eligible balance is what remains after the 25% floor is protected. In effect, up to 75% of your corpus is accessible.

The rule exists for two reasons. First, retirement protection: without a floor, easy withdrawals could empty accounts long before age 58. Second, compounding: the retained 25% keeps earning EPF interest. The declared rate for FY 2024-25 was 8.25%. The rate is announced annually, so verify the current figure on the EPFO website. See how the protected balance grows over time using the EPF Calculator.

Job Loss: How Unemployment Withdrawals Work Now

If you lose your job, you can withdraw up to 75% of your balance soon after job loss. The remaining amount can be withdrawn after one year of unemployment. This staggered approach gives immediate liquidity while preserving part of the corpus in case you rejoin employment and want continuity.

Pension Changes Under EPS 2026

The 36-Month Waiting Period

Previously, a member leaving a job could withdraw EPS contributions after just 2 months of non-employment. The waiting period is now 36 months. This is arguably the most restrictive change in the entire reform. If you were counting on quick EPS withdrawal between jobs, that option is now significantly delayed.

The stated intent is to encourage pension continuity rather than cashing out at every job change. Members with less than 10 years of service can still choose between withdrawing benefits after the waiting period or obtaining a scheme certificate that preserves their service record. Since pension benefits improve with continuous service, the scheme certificate is usually the smarter path anyway.

The 20-Day Claim Deadline With Penalty Interest

A genuinely member-friendly reform: EPFO must now settle a complete pension claim within 20 days, or inform the applicant about deficiencies within the same period. If a complete claim is delayed without valid reason, 12% annual interest becomes payable on the benefit amount, and it is recovered from the salary of the responsible EPFO official. Accountability with teeth.

For employees who opted for higher pension following the Supreme Court ruling on the matter, the additional contribution provisions are now formally built into the scheme.

EPFO 3.0: UPI Withdrawals, WhatsApp Services, Digital Claims

The 2026 scheme formally recognises EPFO’s digital infrastructure. The organisation is rolling out EPFO 3.0, a cloud-based platform intended to speed up claims and improve transparency for over 30 crore members.

UPI withdrawals: EPFO has completed testing a facility for PF withdrawals credited directly to bank accounts through UPI. WhatsApp services: Planned services will let members check PF balance, view the last five transactions, and track claim status through EPFO’s verified account in multiple regional languages. Digital Life Certificates: EPS-95 pensioners can submit DLCs from home through India Post Payments Bank.

Action point: The scheme requires Aadhaar, PAN, and an Aadhaar-seeded bank account for digital claim processing. If your KYC on the UAN portal is incomplete, fix it now. Incomplete KYC will be the single biggest reason for stuck claims under the new digital-first system.

Should You Contribute More Than ₹1,800?

With voluntary contributions now clearly separated, employees earning above ₹15,000 basic face a real decision.

Case for contributing more: EPF interest (8.25% for FY 2024-25) is high for a government-backed, low-risk instrument. Contributions qualify under Section 80C within limits under the old tax regime. Forced saving discipline is genuinely valuable for most people.

Case for contributing only the mandatory amount: Interest on employee contributions above ₹2.5 lakh per year is taxable, which reduces effective returns for high contributors. PF remains less liquid than mutual funds or deposits even with relaxed withdrawal rules. Younger investors with long horizons may earn more in equity, though with higher risk.

There is no single right answer. It depends on your tax regime, risk appetite, and liquidity needs. Compare regimes with the Old vs New Tax Regime Calculator, and weigh alternatives using the PPF vs NPS Comparison Calculator. This article is information, not investment advice.

Project your PF corpus under the new rules.

See year-by-year growth of your contributions, employer share, and interest.

What Employers Must Do Now

Employers face a wider compliance net. A consolidated return in Form V is due within 15 days of the scheme becoming applicable, with employee details including Aadhaar, PAN, UAN, and wage data. The scheme adds one-time, monthly, and event-based electronic filings, ownership disclosures, and contractor compliance. A formal principal employer concept makes the principal employer ultimately responsible where contractors fail to deposit PF. Exempted PF trusts face stricter reporting.

Three time-bound compliance drives were notified alongside the scheme: the Employees’ Enrolment Campaign (EEC) 2026 for previously uncovered employees, Vishwas 2026 for reduction of damages in legacy litigation, and Amnesty 2026 for employers operating exempted private PF trusts. Businesses with past PF gaps should discuss these windows with a labour law consultant.

5 Smart Moves for EPF Members in 2026

Move 1: Complete your KYC today. Aadhaar, PAN, and bank seeding on the UAN portal. Everything digital flows from this.

Move 2: Treat the locked 25% as untouchable retirement money. Mentally account for it as your pension floor, not a restriction imposed on you.

Move 3: Do not drain PF just because withdrawal is easier. Every rupee withdrawn loses decades of compounding at EPF rates. Withdraw for genuine needs only.

Move 4: Prefer scheme certificates over EPS withdrawal at job changes. With the 36-month wait, transferring service is now the practical default, and pension benefits improve with continuous service.

Move 5: Download your PF passbook now. Record your balance before and after the transition so any discrepancy is easy to flag.

Real-Life Example: Priya’s PF Decisions Under the New Rules

Priya, 29, marketing manager in Pune. Basic salary: ₹60,000/month. Current PF balance: ₹6 lakh.

Under the new rules, Priya’s mandatory PF is ₹1,800 per month. Her employer previously deducted 12% of full basic (₹7,200). Her company has kept the existing structure, so nothing changes in her payslip. She confirmed this with HR instead of assuming.

Her sister’s wedding is in December. Under the old rules, using a marriage withdrawal would have consumed one of just 3 lifetime education-plus-marriage chances. Now she has 5 marriage withdrawals available separately. She can withdraw up to her eligible balance, which is her corpus minus the protected 25% (₹1.5 lakh stays locked). She withdraws ₹2 lakh and leaves the rest compounding.

In March she plans to switch jobs. Instead of withdrawing EPS (now blocked for 36 months anyway), she transfers her account via UAN and keeps her pension service continuous. Ten years from now, that continuity directly increases her pension under the unchanged formula.

Plan Your Complete Retirement Strategy

PF is one pillar of retirement, not the whole plan. Project your provident fund corpus with the EPF Calculator and your overall retirement number with the Retirement Calculator. Compare fixed income options using the PPF Calculator and NPS Calculator, and estimate your exit benefits with the Gratuity Calculator.

Check how PF deductions affect your payslip with the Take Home Salary Calculator and your tax outgo with the Income Tax Calculator. Before making a housing withdrawal, compare outcomes with the Home Loan EMI Calculator and Buy vs Rent Calculator. Instead of raiding PF for emergencies, build a buffer using the Emergency Fund Calculator.

Explore all free tools at PlanMyReturns Calculators. Every calculation follows transparent methodology and assumptions you can verify.

Frequently Asked Questions: EPF Scheme 2026