A complete guide to Loan EMI Calculator with real cost comparison between home loan and car loan in India for FY 2026-27. Understand EMI formula, total interest paid, prepayment impact, tax benefits, and the smartest borrowing strategy for Indians.

An EMI calculator helps you compute the exact monthly installment, total interest, and total payable amount on any loan before signing the agreement. The same EMI formula applies to home loans and car loans. But the real cost differs dramatically because of interest rates, tenure, tax benefits, and asset behavior.

Most Indians take both loans during their lifetime. A car loan in their late 20s, a home loan in their 30s. But few understand the staggering difference in real cost between the two. A ₹10 lakh car loan and a ₹50 lakh home loan look very different on paper, but the cost-per-rupee borrowed tells an even more interesting story.

In this guide, we break down the EMI formula, compare home loan vs car loan costs side by side with real numbers for 2026, and reveal which loan you should prepay first to save the most money.

Quick rule: Use the EMI Calculator for any loan. For specific scenarios, use the Home Loan EMI Calculator or Car Loan Calculator.

How EMI Calculation Works: The Formula

Every loan EMI in India is calculated using the same standard formula. Banks, NBFCs, and HFCs all use this method. The only variables are the loan amount, interest rate, and tenure.

Where P = Principal, R = Monthly interest rate, N = Total months

Breaking down the formula: If you take a ₹50 lakh home loan at 8.50% annual interest for 20 years, the monthly rate is 8.50/12/100 = 0.00708. Total months = 240. Plug into the formula and your EMI = ₹43,391/month. Total payable = ₹1,04,13,840. Total interest = ₹54,13,840.

Manual calculation is painful. The EMI Calculator on PlanMyReturns does this instantly with a year-by-year amortization schedule showing how much of each EMI goes to principal vs interest.

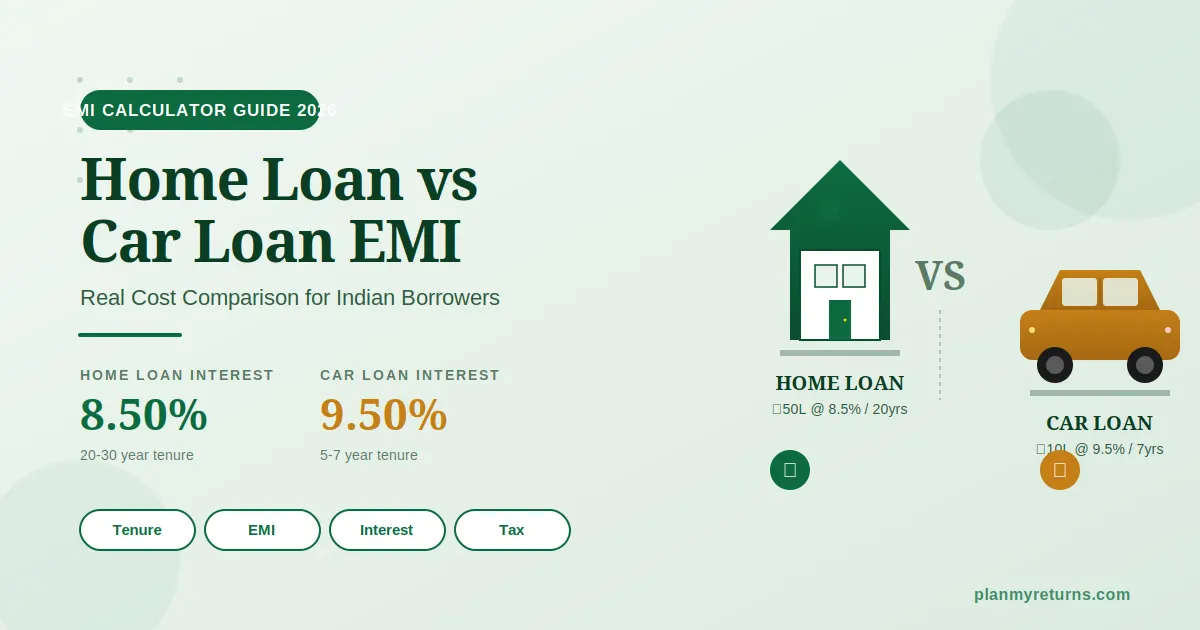

Home Loan vs Car Loan: Real Cost Comparison 2026

Let’s compare two real-world scenarios that most Indians encounter. A ₹50 lakh home loan and a ₹10 lakh car loan, both at current 2026 interest rates.

The shocking takeaway: A home loan ends up costing you 108% of the principal in interest over 20 years. You essentially pay for two homes when you finance one. The car loan only costs 37% in interest because of the shorter tenure. But the car depreciates while paying interest. The house appreciates.

Calculate your exact figures using the Home Loan EMI Calculator and Car Loan Calculator based on your loan amount and tenure.

Calculate your exact loan EMI in seconds.

Try different tenures and rates to find the most affordable EMI for your budget.

Side-by-Side: Home Loan vs Car Loan

Here’s the complete comparison across every parameter that matters when choosing or evaluating a loan.

Verdict: Home loans win on almost every parameter except down payment percentage. Car loans should be a last resort. If you must take one, keep the tenure short and the loan amount minimal.

Tax Benefits: Home Loan’s Hidden Superpower

This is where home loans crush car loans. Indian taxpayers can claim three different deductions on a home loan. Car loans for personal use offer zero tax benefit.

Section 80C: Principal Repayment Deduction

The principal portion of your home loan EMI qualifies under Section 80C. The deduction limit is ₹1,50,000 per year, shared with other 80C investments like ELSS, PPF, EPF, and life insurance premiums.

Catch: Available only if you do not sell the property within 5 years of possession. Otherwise, deductions claimed in earlier years get reversed and added back to your income.

Section 24(b): Interest Deduction on Self-Occupied Property

You can claim up to ₹2 lakh per year as a deduction on home loan interest paid for a self-occupied property. For a let-out (rented) property, the entire interest paid is deductible without any cap, subject to the ₹2 lakh loss-from-house-property limit.

Critical 2026 update: The self-occupied property interest deduction limit of ₹2 lakh remains unchanged in the latest Finance Act. Use the Income Tax Calculator to see how this lowers your taxable income.

Section 80EEA: Extra ₹1,50,000 for Affordable Housing

First-time home buyers purchasing affordable housing (stamp duty value up to ₹45 lakh) can claim an additional ₹1.5 lakh deduction on home loan interest under Section 80EEA. This is over and above the ₹2 lakh limit under Section 24(b).

Combined benefit: ₹1.5L (80C) + ₹2L (24b) + ₹1.5L (80EEA) = up to ₹5 lakh tax deduction per year on a single home loan. At 30% tax bracket, that’s ₹1,56,000 in annual tax savings (with cess).

How much tax will you save with your home loan?

Calculate exact tax savings under both old and new tax regime.

The Hidden Cost: Total Interest Paid Over Tenure

EMI looks small. But total interest paid is shocking. Most borrowers focus on monthly EMI and ignore the lifetime cost. Here’s what you actually pay across different scenarios:

The 10 vs 30 year reality: A 30-year tenure has only ₹3,000 lower EMI than 20 years. But you pay ₹34 lakh extra in interest. That’s 64% more interest for marginal EMI relief. Always pick the shortest tenure your monthly budget allows.

Prepayment: The Real Money-Saver

Home loan prepayment is the single most powerful way to save lakhs in interest. Most Indians don’t understand its impact. A small ₹1 lakh prepayment in year 2 can save you ₹3 to 4 lakh in total interest. Here’s why:

How prepayment math works: In the early years of a 20-year home loan, almost 75% of your EMI goes to interest. Only 25% reduces principal. When you prepay, every rupee directly reduces principal, eliminating compound interest on that amount for the remaining tenure.

Real example: ₹50L home loan at 8.5% for 20 years. If you prepay ₹2 lakh in year 3, you save approximately ₹6.8 lakh in total interest and finish the loan 14 months earlier. Calculate your exact prepayment savings using the Loan Prepayment Calculator.

Prepay Car Loan or Home Loan First?

Always prepay the car loan first. Here’s why:

Reason 1: Higher interest rate. Car loans charge 9 to 11% vs home loans at 8.40 to 9.50%. Higher rate = more savings from prepayment.

Reason 2: No tax benefit on car loan. You don’t lose any deduction by prepaying car loan. With home loan, you lose Section 24(b) interest deduction proportionally.

Reason 3: Depreciating asset. Your car loses 15 to 20% value every year. Paying interest on a depreciating asset is wealth destruction. Property typically appreciates.

Reason 4: Effective home loan rate is lower. After 30% tax savings on Section 24(b), an 8.5% home loan effectively costs only about 6% post-tax. Car loan stays at full 9.5%.

5 Smart EMI Strategies for Indian Borrowers

Strategy 1: Keep total EMI under 40% of monthly income. If your monthly take-home is ₹1,00,000, your combined EMI for all loans should not exceed ₹40,000. Lenders will approve more, but discipline prevents EMI stress. Calculate your eligibility using the Loan Eligibility Calculator.

Strategy 2: Choose floating rate over fixed for home loans. Home loan rates in India have been falling since 2024. RBI repo rate cuts get passed to borrowers via floating rates. Fixed rates lock you into higher pricing. Floating rate home loans have zero prepayment penalty per RBI rules.

Strategy 3: Make one extra EMI payment per year. Pay 13 EMIs per year instead of 12. On a 20-year ₹50L home loan, this single habit reduces tenure by 4 years and saves approximately ₹14 lakh in interest. Use the Loan Prepayment Calculator to verify.

Strategy 4: Avoid car loan if you can buy car cash. If you have ₹10 lakh in mutual funds returning 12%, taking a car loan at 9.5% looks profitable. But factor in market volatility, taxation on gains, and emotional stress of EMIs. For a depreciating asset, cash purchase usually wins.

Strategy 5: Don’t extend tenure to reduce EMI. Banks offer to “reduce your EMI” by extending tenure during a loan reset. This saves you a few thousand in monthly EMI but costs lakhs in extra interest. Always negotiate for lower rate, not longer tenure.

Real-Life Example: Rohit’s Loan Journey

Rohit, 32, IT Manager in Hyderabad. Monthly take-home: ₹1,20,000.

Rohit took a ₹10 lakh car loan in 2024 at 9.5% for 7 years. EMI: ₹16,344. He took a ₹60 lakh home loan in 2026 at 8.5% for 20 years. EMI: ₹52,069.

Total monthly EMI: ₹68,413. That’s 57% of his take-home. Bank approved it. But Rohit decided to prepay aggressively.

Rohit’s plan: Pay extra ₹50,000 every Diwali bonus and ₹1,00,000 every annual bonus, all directed to the car loan first. Result: Car loan closed in 4 years instead of 7. Saved ₹2.1 lakh in interest. After car loan closure, that ₹16,344 EMI now goes to home loan prepayment, accelerating it by 6 years.

Total savings: ₹2.1 lakh on car loan + approximately ₹38 lakh on home loan = over ₹40 lakh saved across his lifetime. Calculate your own prepayment plan using the Loan Prepayment Calculator.

Plan your prepayment strategy like Rohit.

See exact interest savings and tenure reduction with any prepayment amount.

Plan Your Complete Loan Strategy

EMI calculations are just the starting point. Smart borrowing requires comparing multiple loan types and tenures. Use these calculators on PlanMyReturns to plan your borrowing.

Calculate any loan EMI with the universal EMI Calculator. For specific loans, use the Home Loan EMI Calculator, Car Loan Calculator, Personal Loan Calculator, Business Loan Calculator, or Education Loan Calculator. Check your eligibility first using the Loan Eligibility Calculator.

Before buying a home, run a Buy vs Rent Calculator analysis. For specific banks, use the LIC Home Loan EMI Calculator. Compare with the Home Loan Overdraft Calculator if you have lumpy savings.

Explore all free financial calculators at PlanMyReturns Calculators. Every calculation follows transparent methodology and assumptions you can verify.

Frequently Asked Questions: Loan EMI