The complete SIP calculator guide for Indian investors. Know exactly how much to invest monthly to build a ₹1 crore, ₹2 crore, or ₹5 crore corpus. Real scenarios with ₹5K, ₹10K, ₹15K, and ₹25K monthly SIPs over 10, 15, 20, and 25 years.

Becoming a crorepati through SIP is not about how much money you have. It is about how early you start and how disciplined you stay. A 25-year-old investing just ₹3,100 per month in equity mutual funds can retire with ₹1 crore at age 50. The same ₹1 crore goal at age 40 requires ₹8,700 per month if you only have 20 years to invest. Time is the most powerful weapon in wealth creation.

In this guide, we break down exactly how much SIP you need based on your target corpus and investment duration. We use the standard 12% annual return assumption, which matches the long-term historical average of Indian equity markets. Every number below is calculated with real compound interest formulas, not marketing promises.

The biggest enemy of wealth is not the market. It is delay. Waiting 5 years to start a SIP can cost you over 40% of your final corpus. Let us show you why.

Quick Reality Check. 15-year rolling returns of Nifty 50 from 2005 to 2025 averaged 12.1% per annum. This is the basis for our 12% assumption. For conservative planning, use 10%. For aggressive projections, never exceed 15%.

How SIP Makes You a Crorepati: The Math Behind It

SIP (Systematic Investment Plan) works on three simple principles. Rupee cost averaging means you buy more mutual fund units when prices are low and fewer when they are high, reducing your average cost over time. Compounding means your returns start earning returns. Discipline means you invest every single month, regardless of whether the market is up or down.

Here is the SIP formula that calculates your future corpus:

FV = P × [((1 + r)^n − 1) / r] × (1 + r)

Where: FV = future value, P = monthly SIP amount, r = monthly return rate (annual ÷ 12), n = total months. Or simply use the SIP Calculator and skip the math.

But the formula is not what matters. What matters is this truth: the first 10 years of your SIP feel slow. Years 11 to 20 feel magical. Years 21 to 30 are where wealth is actually built. Most people quit in year 3 because returns look boring. Do not be that person.

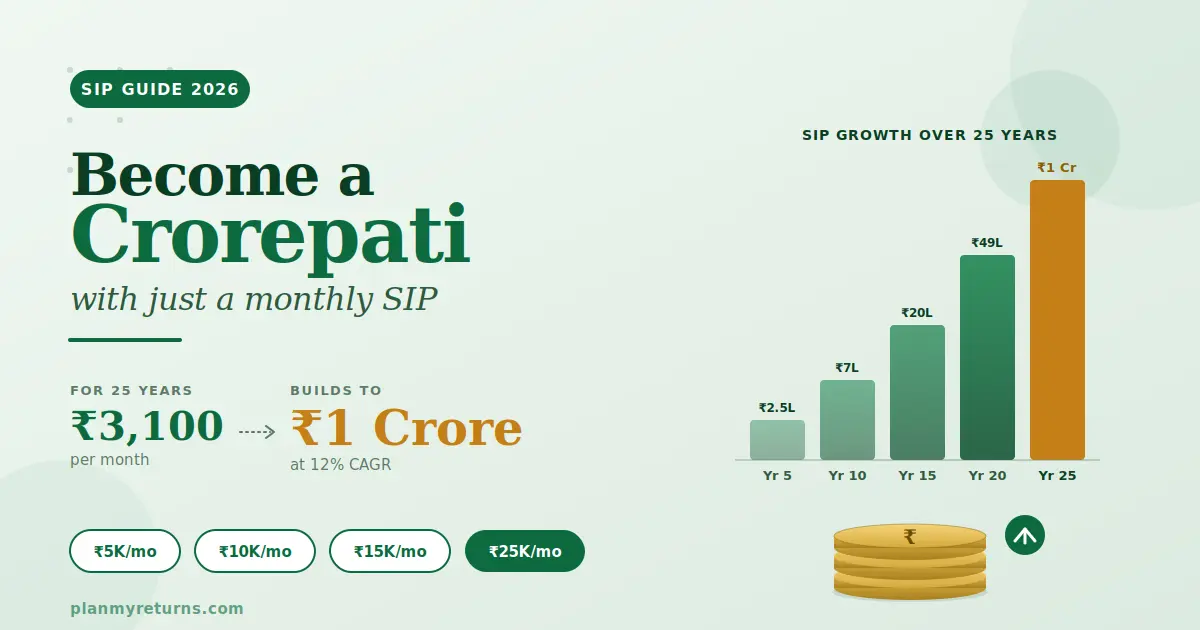

₹1 Crore SIP: Exact Monthly Amount You Need

This is the question everyone asks. The answer depends entirely on how many years you have. Below are the exact SIP amounts needed for a ₹1 crore corpus at 12% annual returns:

Read that last card again. ₹3,100 per month for 25 years turns into ₹1 crore. You invest only ₹9.3 lakh total. The market gives you the other ₹90.7 lakh. This is the power of starting early. A 25-year-old can become a crorepati by investing just ₹100 per day.

See your exact crorepati SIP amount.

Try different amounts, tenures, and return rates instantly.

Real SIP Scenarios: ₹5K, ₹10K, ₹15K, ₹25K Monthly

Not everyone can save ₹43,500 per month. Most Indian investors start with smaller amounts and scale up over time. Here is what realistic SIP amounts grow into over 20 years at 12% annual returns:

The “Just Starting Out” SIP

Perfect starting point for fresh graduates and young professionals. Automate this and forget about it. Step up by 10% every year when you get a salary hike.

The “Getting Serious” SIP

Nearly a crorepati in 20 years. Add a step-up of 10% per year and you cross ₹1.5 crore easily. This is the sweet spot for most Indian salaried employees in their late 20s and 30s.

The “Wealth Builder” SIP

Crorepati in under 20 years. Ideal for professionals earning ₹10 lakh+ per year who want a solid retirement corpus. Add NPS on top for maximum tax efficiency.

The “Early Retirement” SIP

Path to FIRE (Financial Independence, Retire Early). A 25-year-old investing ₹25K/month can retire at 45 with ₹2.5 crore. Pair this with our FIRE Calculator to map your exact retirement timeline.

The Cost of Delay: Why Starting Today Matters

Look at this brutal comparison. Two friends, both aiming for ₹1 crore at age 50. Rahul starts SIP at 25. Amit starts at 35. Both assume 12% returns.

Amit had to invest ₹26.7 lakh more from his own pocket just because he started 10 years late. Rahul’s monthly SIP is 6.5x smaller. That 10-year head start is worth nearly 27 lakhs in savings. The best day to start SIP was 10 years ago. The second best day is today.

Step-Up SIP: The Crorepati Accelerator

Most people start a ₹5,000 SIP at 25 and never increase it. By 35, their salary has tripled but their SIP is still ₹5,000. This is a massive wealth leak. Step-up SIP means increasing your SIP amount by a fixed percentage (usually 10%) every year.

₹10,000 SIP with 10% Annual Step-Up

Just a 10% annual step-up more than doubles your corpus. You become a crorepati years earlier. And the increase feels painless because your salary grows faster than 10% per year anyway.

See how step-up SIP builds your wealth.

Play with step-up percentages and see the compounding effect live.

Which Mutual Funds to Pick for Your Crorepati SIP

The fund you choose matters almost as much as the SIP amount. Here is a framework based on your investment horizon:

Disclaimer: Fund names above are historical performers, not recommendations. Past returns do not guarantee future returns. Always check 5-year and 10-year rolling returns, expense ratio, and fund manager tenure before investing. Consult a SEBI-registered advisor for personalized advice.

Real-Life Example: Ankit’s Journey to ₹1 Crore

Ankit, 28, Product Manager in Pune. Salary: ₹12,00,000 per year. Goal: ₹1 crore by age 45.

Ankit has 17 years until his target age. At 12% returns, he needs approximately ₹14,200 per month to hit ₹1 crore by 45.

Instead of a fixed SIP, Ankit chooses step-up SIP: ₹10,000 per month starting now, with 10% annual increase. Year 1: ₹10,000/month. Year 5: ₹14,641. Year 10: ₹23,579. Year 17: ₹45,950.

His projected corpus: ₹1.37 crore by age 45. That is 37% more than his goal, with the same starting amount. All because he committed to a small annual step-up.

Ankit splits his SIP: ₹6,000 in Parag Parikh Flexi Cap, ₹3,000 in Mirae Asset Large Cap, ₹1,000 in a midcap fund for growth. He reviews once a year. That is it. Use the SIP Calculator to model your own Ankit-style plan.

5 SIP Mistakes That Destroy Your Crorepati Dream

Mistake 1: Stopping SIP when market falls. This is the single biggest wealth destroyer. When the market falls 20%, your SIP is buying units at a discount. Stopping your SIP during a crash is like refusing to buy groceries during a sale.

Mistake 2: Chasing last year’s best performing fund. The fund that topped charts last year is rarely the one that does it next year. Stick to consistent performers with 5-10 year track records. Performance chasing kills long-term returns.

Mistake 3: Not doing step-up SIP. Your SIP amount in 2026 should not be the same as 2020. Salary grows. SIP must grow too. Even a 5% step-up boosts your corpus by 30-40% over 20 years.

Mistake 4: Mixing insurance with investment. ULIPs and endowment plans give 4-6% returns. SIP in equity mutual funds gives 12%+. For life cover, buy cheap term insurance. For wealth, use SIP. Never mix the two.

Mistake 5: Breaking SIP for short-term goals. Using your SIP corpus to buy a bike, renovate a home, or take a vacation destroys compounding. Keep a separate emergency fund. Check how much you need using the Emergency Fund Calculator.

Beyond ₹1 Crore: Planning for Real Wealth

Here is a truth most financial content avoids. ₹1 crore in 2046 will buy what ₹30 lakh buys today, assuming 6% inflation. If you are 30 today and retire at 60 with ₹1 crore, that money may not fund a comfortable retirement.

For real financial freedom, aim for 25-30 times your annual expenses as your retirement corpus. If you spend ₹6 lakh per year today, you need ₹1.5 crore to ₹1.8 crore in today’s money, which is ₹5-9 crore in 2050 terms.

Plan your exact retirement corpus using the Retirement Calculator. Build a lumpsum investment strategy alongside SIP using the Lumpsum Calculator. Track your net worth progress with the Net Worth Calculator.

Explore all free SIP and mutual fund calculators at PlanMyReturns Calculators. Every calculation follows transparent methodology and assumptions you can verify yourself.

Your crorepati journey starts with one calculation.

Know exactly what SIP you need. No guessing. No marketing.

Frequently Asked Questions: SIP for Crorepati Goal